Yahoo Finance

Yahoo Finance Newell's (NWL) DYMO Line Unveils Three LabelWriter Printers

Newell Brands Inc.’s NWL DYMO product line introduced three LabelWriter machines as part of its product innovation efforts. The new products are — LabelWriter 550, which is an ink-free label printer; the high-speed printer LabelWriter 550 Turbo, with LAN network connectivity; and LabelWriter 5XL, which can print extra-large labels up to four inches wide. The move is also in sync with consumers’ growing demands for office and at-home printing supplies.

All three models support PC and Mac operating systems and can be used for business purposes, including printing labels for addresses, mailing, shipping, file folders, visitor management, asset tracking, inventory and price tags. The products feature direct thermal printing technology and the new Automatic Label Recognition, which helps detect the label size, type, color and advanced reliability, and helps prevent the possibility of misprinting labels. Customers can also track remaining labels, thus, reducing unplanned downtime.

DYMO’s new products are not only easy to use but also sustainable. Its authentic LabelWriter paper labels are made up of FSC certified materials and label box packaging uses 80% recycled paper.

What’s More?

Newell has been witnessing a recovery in the Writing Business with core sales growth in the unit in second-quarter 2021. Strength across all regions, school re-openings and the demand for key categories such as pens, presentation markers, permanent markers and highlighters remained upsides. Within the unit, the gel pen category and “Boy, do I love that pen” also act as key growth drivers. This marked the second consecutive quarter of strong POS growth in the Writing business. Going ahead, management remains optimistic about the back-to-school season and is on track for long-term growth on the back of robust merchandising plans.

With the acceleration of the vaccine programs, the resurgence in in-store consumption trends also bodes well. In second-quarter 2021, the company witnessed healthy consumption trends in the United States, as business trends normalize. Sales growth in brick-and-mortar stores outpaced digital sales in the reported quarter, as it lapped a period of store closures and lockdowns in the year-ago quarter.

Newell’s solid online show has been strong for some time now due to customers’ persistent shift to the online platform. As a result, e-commerce sales grew in the mid-single digits, accounting for roughly 20% of total sales in the second quarter. Going forward, the company expects digital penetration to increase despite the potential quarterly fluctuations due to the lapping of the extravagant digital sales witnessed in 2020 due to store closures.

Management raised the 2021 sales view and issued upbeat third-quarter guidance on its last reported quarter’s earnings call. The company anticipates sales of $10.1-$10.35 billion for 2021 compared with the earlier mentioned $9.9-$10.1 billion. Core sales growth is likely to be 7-10%, up from the previously stated 5-7%. Normalized earnings per share are still forecast at $1.63-$1.73 for the year. For third-quarter 2021, net sales are envisioned to be $2.7-$2.78 billion, with core sales ranging from flat to up 3% year over year. Normalized earnings are likely to be 46-50 cents a share.

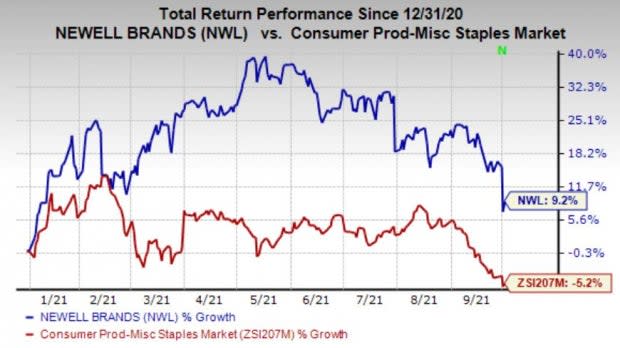

We note that shares of this Zacks Rank #3 (Hold) stock have gained 9.2% year to date against the industry’s decline of 5.2%.

Image Source: Zacks Investment Research

However, elevated advertising and promotional expenses related to product launches and omnichannel investments remain concerning. It also witnessed higher transportation and labor costs in the second quarter. Management expects inflationary pressures to be at its peak in the third quarter. This is likely to hurt margins. The third-quarter normalized operating margin is forecast to be 10.3-10.8%, suggesting a decline from the prior-year quarter’s reported figure of 14.9%.

Better-Ranked Stocks to Consider

Leslies LESL has a Zacks Rank #1 (Strong Buy). It has a long-term earnings growth rate of 32.8%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Albertsons Companies ACI, a Zacks Rank #2 (Buy) stock, has an expected long-term earnings growth rate of 12%.

Conagra Brands CAG currently has a long-term earnings growth rate of 7% and a Zacks Rank #2.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Newell Brands Inc. (NWL) : Free Stock Analysis Report

Albertsons Companies, Inc. (ACI) : Free Stock Analysis Report

CONAGRA BRANDS (CAG) : Free Stock Analysis Report

Leslies, Inc. (LESL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research