Yahoo Finance

Yahoo Finance Molson Coors (TAP) Stock Down on Q2 Earnings & Sales Miss

Molson Coors Brewing Company TAP reported a dismal second-quarter 2019 results, wherein top and bottom lines missed estimates and declined year over year. This marked the company’s second straight earnings miss and third consecutive negative sales surprise. The top line was impacted by soft volume that stemmed from unfavorable weather and weak industry demand across the majority of its geographies in May and June.

Following the soft results, shares of Molson Coors declined nearly 6.9% in the pre-market trading session. Though this Zacks Rank #3 (Hold) company’s shares have gained 1.3% year to date, it has underperformed the industry’s 23.2% growth.

Delving Deeper

Molson Coors’ underlying adjusted earnings of $1.52 per share declined 19.1% year over year and missed the Zacks Consensus Estimate of $1.65. The decline was attributed to soft volume, cost inflation in all segments, higher marketing expenses owing to ongoing investments to support premiumization and innovation efforts, and lower G&A benefits from last year. This was partly negated by positive global net pricing in all segments, gain on the sale of Montreal brewery and cost savings.

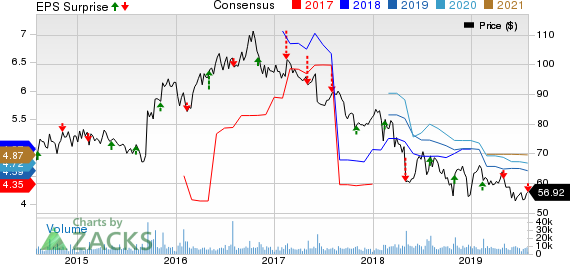

Molson Coors Brewing Company Price, Consensus and EPS Surprise

Molson Coors Brewing Company price-consensus-eps-surprise-chart | Molson Coors Brewing Company Quote

The aforementioned factors also led to a decline in the company’s underlying EBITDA, which moved down 9.2% to $1,098.3 million year over year. Further, underlying EBITDA slipped 12.8% year over year in constant currency.

Net sales declined 4.4% to $2,948.3 million, missing the Zacks Consensus Estimate of $3,014 million. The top-line miss can be attributed to lower volumes, partly negated by higher global pricing and a favorable sales mix. On a constant-currency basis, net sales fell 2.9% on soft volume, partially offset by solid net sales per hectoliter growth.

Notably, net sales per hectoliter rose 2.7% on a reported financial-volume basis. Moreover, net sales per hectoliter on brand-volume basis improved 3.7% in constant currency, owing to favorable pricing in all segments and positive global mix due to the company’s focus on premiumizing its portfolio.

Molson Coors’ worldwide brand volume declined 5.6% and financial volume fell 7% to 25.8 million hectoliters. This decline was mainly attributed to volume declines in all segments. Soft volume across segments stemmed from unfavorable weather and weak industry demand conditions across the majority of its geographies in May and June.

Segmental Details

The company operates through the following geographical segments.

Canada: Molson Coors’ Canada net sales declined 6.1% to $373 million on a reported basis and 2.9% in constant currency. Net sales per hectoliter (brand-volume basis) rose 2.7% in constant currency due to favorable pricing. Further, Canada brand volume fell 5.1% and financial volume decreased 5.3%, owing to industry declines. Underlying EBITDA moved down 26.7% to $70.5 million year over year, with a constant-currency decline of 25.4%. This decline mainly stemmed from the impacts of soft volume, unfavorable mix and cost inflation along with higher M&A expenses.

United States: Molson Coors now has complete ownership rights to all the brands in the MillerCoors portfolio for the U.S. market. Net sales for the segment dropped 2.9% to $2,011.7 million on reported and constant currency basis. However, domestic net sales per hectoliter (on a brand-volume basis) improved 3.6% due to higher net pricing.

However, U.S. brand volume decreased 4.8%, thanks to industry declines. Sales-to-wholesalers (STWs) volume, excluding contract brewing, declined 6.7% due to lower brand volume and quarterly timing of wholesaler inventories. The segment’s underlying EBITDA declined 8.2% year over year to $529.1 million.

Europe: The segment reported net sales decline of 8.1% to $538.5 million and decrease of 2.4% in constant currency, thanks to soft volumes. However, net sales per hectoliter (brand-volume basis) in Europe rose 4.3% in constant currency due to positive pricing and favorable sales mix. Europe brand and financial volume declined 6.5% and 6.9%, respectively, thanks to unfavorable weather and soft industry demand along with the absence of the benefit of higher consumption from the World Cup in the prior year. Underlying EBITDA declined 22.8% year over year to $104.9 million, with 18.4% decrease in constant currency.

International: Net sales for the segment declined 13.3% to $58.9 million and 12.1% in constant currency. This was driven by lower net sales per hectoliter and brand volume. Net sales per hectoliter, on a brand-volume basis, dipped 0.6%, thanks to the shift to local production in Mexico. This was partly negated by positive pricing and geographic shift. International brand volume declined 11.9%, backed by balancing of higher pricing for Coors Light in Mexico, with supply-chain constraints in India. This was partly offset by double-digit growth in several focus markets. The segment’s underlying EBITDA was $5.8, reflecting a year-over-year decline of 10.8% on reported and constant currency basis.

Other Financial Updates

Molson Coors ended the reported quarter with cash and cash equivalents of $490.2 million and total debt of $9,553 million. This resulted in net debt of $9,062 million as of Jun 30, 2019.

Net cash used in operating activities for the first half of 2019 was $828 million. Underlying free cash flow was $560.7 million.

Outlook

Management reiterated its guidance for 2019. Molson Coors anticipates generating cost savings of roughly $205 million in 2019, remaining on track with the target of generating total cost savings of $700 million during the 2017-2019 period. In 2019, the company expects to deliver underlying free cash flow of around $1.4 billion (plus or minus 10%).

Capital spending is expected to be roughly $700 million (plus or minus 10%). Underlying tax rate for the year is likely to be 18-22%. Additionally, net interest expenses are projected to be $300 million (plus or minus 5%).

Further, consolidated underlying COGS per hectoliter are likely to increase in a mid-single digit on a constant-currency basis. The company estimates a double-digit percentage increase for underlying EBITDA in constant currency for the International business.

It is on track with the plan to reinstitute a dividend payout target of 20-25% of the prior year’s underlying EBITDA. It expects to achieve this target with the payout of its next quarterly dividend of 57 cents that is payable Sep 13, 2019.

Don’t Miss These Better-Ranked Alcohol Stocks

The Boston Beer Company Inc. SAM, with long-term earnings per share growth rate of 10%, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Castle Brands, Inc. ROX witnessed positive revisions for the current-year EPS estimates in the last 30 days. The stock carries a Zacks Rank #2 (Buy) at present.

Craft Brew Alliance, Inc. BREW, also a Zacks Rank #2 stock, reported positive earnings surprise of 20.8% in the last reported quarter.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Boston Beer Company, Inc. (SAM) : Free Stock Analysis Report

Craft Brew Alliance, Inc. (BREW) : Free Stock Analysis Report

Molson Coors Brewing Company (TAP) : Free Stock Analysis Report

Castle Brands, Inc. (ROX) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research