Yahoo Finance

Yahoo Finance What Investors Need to Know About Goldcorp Stock

Those seeking to invest in gold have several options, including buying the precious metal, gold ETFs, or gold mining stocks such as Goldcorp Inc. (NYSE: GG). While in theory, all those options would benefit from the rising price of gold, investors risk missing out on a gold run unless they invest in the actual physical metal or a gold ETF that tracks it. That's because gold mining stocks like Goldcorp add in a layer of operational risk that can cause them to underperform the price of gold if they make a misstep.

In fact, that's just what has happened with Goldcorp's stock over the last decade, where it has lost nearly two-thirds of its value even though gold has risen almost 50%. That underperformance isn't uncommon among gold mining stocks, which Wall Street has punished in recent years due to their value-destroying expansion efforts. That underperformance, however, drove Goldcorp to work on an ambitious strategy to create value for investors by making targeted investments to boost profitability and, hopefully, its stock price.

Image source: Getty Images.

Digging into Goldcorp

Goldcorp, unsurprisingly, makes most of its money mining gold. In 2017, the company produced nearly 2.6 million ounces of gold, making it the fifth largest gold producer in the world. Overall, its gold mining activities supplied the company with $2.5 billion in revenue that year, good for about 74% of the total. The rest of its revenue came from zinc (12% of 2017's sales), silver (11%), and other metals like lead and copper (3%).

Goldcorp mines the bulk of its gold from several large-scale operations in seven countries across North and South America. The biggest contributor is the Penasquito mine in northwest Mexico, which supplied 33% of the company's total production in 2017 (including most of its silver, lead, and zinc) and 18% of revenue. Furthermore, it is among the company's lowest-cost mines, delivering an all-in sustaining cost (AISC) of just $370 an ounce. For comparison's sake, the company's average AISC that year was $825 an ounce.

Another major contributor is the Cerro Negro mine in Argentina, which is the company's newest, delivering its first production in 2014. It contributed 14% of Goldcorp's production in 2017 and 18% of its revenue, at below-average costs of $684 an ounce.

One other noteworthy mine is Pueblo Viejo in the Dominican Republic, which the company owns in a joint venture (JV) with Barrick Gold (NYSE: ABX). It's one of the largest gold mines in the world. Overall, Goldcorp owns a 40% stake in the JV, which supplied the company with 14% of its production and 17% of its revenue in 2017.

In addition to those operating mines, Goldcorp has several in development. One of the largest is NuevaUnion, which is a 50/50 JV with Teck Resources on one of the largest undeveloped copper-gold-molybdenum projects in Latin America. The proposed Chilean mine is still in a pre-feasibility study and, therefore, several years away from development.

Another major long-term project is Norte Abierto, which is also a 50/50 JV in Chile -- this time with Barrick Gold -- on one of the largest gold-copper discoveries in South America. Goldcorp just brought this project into its portfolio in 2017 after buying out Kinross Gold's (NYSE: KGC) 25% stake as well as a 25% interest from Barrick Gold.

Building a gold mining giant one deal at a time

While Goldcorp was the world's fifth largest producer in 2017, it didn't get there overnight. The company started out in 1994 by operating two mines: Wharf in the U.S. (which it sold to Coeur Mining in 2015) and the Red Lake mine in Canada, which it still owns to this day. The company would go on to make its first transformational acquisition nearly a decade later, buying Wheaton River in a $2 billion deal that doubled its production to more than one million ounces on an annual basis. The next year Goldcorp acquired several additional mines that have become key pillars for the company, including adding Penasquito and its 40% stake in Pueblo Viejo as well as others in Canada, Guatemala, and Honduras. Goldcorp would go on to acquire more mines and mining companies in the years that followed, as well as invest heavily in developing new gold mines.

While this expansion grew Goldcorp's gold production up to nearly 3.5 million ounces by 2015, the company piled on a mountain of debt to its balance sheet in the process, hitting more than $3.6 billion by the middle of that year. The weight of that debt, along with sliding gold prices, pushed Goldcorp's stock down from a peak of around $55 a share in 2011 to the low teens by early 2018.

Gold price in U.S. dollars data by YCharts.

Goldcorp has been working to trim its debt in recent years by selling non-core assets. As noted earlier, the company parted with its legacy Wharf mine in 2015 as one of many steps to unlock the value of its portfolio by focusing on its core assets and paying down debt. The company would go on to sell several more mines and other assets as part of a major restructuring through 2016 to refocus on its best properties. While this decision resulted in gold production falling by 1 million ounces from the peak, the company entered 2018 with just under $2 billion in debt, putting it in a better position to deliver profitable growth in the future.

A new way forward for Goldcorp

Goldcorp's transformation efforts culminated in early 2017 when the company unveiled an ambitious five-year growth program dubbed 20/20/20. The plan would see the company:

Increase production by 20%, from 2.5 million ounces of gold expected in 2018 prodiuction up to 3 million ounces by 2021.

Reduce AISC by about 20% to $700 an ounce by 2021.

Grow gold reserves 20% from 50 million ounces in 2016 to 60 million ounces by 2021.

Driving Goldcorp's strategy are targeted investments aimed at increasing output and reducing costs at its core mines. For example, the company is pouring $420 million into its Penasquito mine over the next few years to improve its processing facilities. One of the projects will enable Goldcorp to recover 40% of the gold that currently sits as waste in the tailings (which are materials left over after processing). Meanwhile, the company is developing new mines within existing complexes to increase production. These investments will help drive down costs, while also expanding its gold reserves.

Furthermore, Goldcorp's plan would see the company generate increasing free cash flow, enabling it to steadily reduce net debt, with the aim of driving it toward zero within five years. That will give the company the financial flexibility to invest in its next stage of expansion projects, including the two JVs in Chile.

Does this make Goldcorp's stock a buy?

In the past, Goldcorp focused on creating one of the largest gold producers in the world by building and buying mines to move up the leaderboard. While the company did build a gold mining empire, that approach didn't create value for investors. In fact, Goldcorp's stock has underperformed the S&P 500 since its formation, with truly abysmal performance after going on its buying binge in 2004, considering that shares are down 2% in the nearly 14 years since that deal, even though gold is up almost 200%.

Goldcorp's vision for tomorrow is quite different from that of the past, driven by its 20/20/20 strategy. That's because instead of focusing on growing the size of the company, this plan aims to increase profitability, which is the key to expanding shareholder value. If the company hits its target, it should generate more than $2.5 billion in annual EBITDA by 2021, up nearly 50% from the $1.7 billion it pulled in during 2017 -- assuming a stable gold price, which is no sure thing. However, if gold cooperates, this plan to grow profitability should make Goldcorp a more valuable company going forward. That potential to create value for investors in the coming years makes Goldcorp a compelling gold stock to consider buying in 2018.

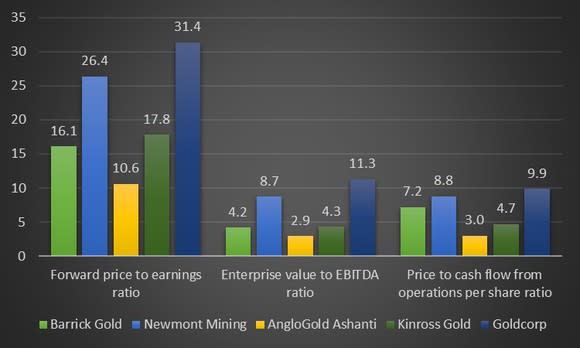

An expensive stock

Though it's worth noting that even with the company's abysmal stock performance over the past several years, shares trade at a more expensive relative valuation versus the four gold miners ahead of it on the production leaderboard:

Data source: YCharts. Chart by the author.

As this chart shows, Goldcorp's stock isn't just marginally more expensive than stocks of rival miners; it's by far the most expensive in the group across several valuation metrics. Because of that, investors need to weigh the upside potential of the company's 20/20/20 plan against the possibility that it could still underperform its cheaper rivals in a stable-to-rising gold price environment, unless investors remain willing to continue paying a premium for Goldcorp's stock. Given that trade-off, investors should first take a closer look at the miner's cheaper rivals before making any decisions.

More From The Motley Fool

Matthew DiLallo has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.