Yahoo Finance

Yahoo Finance Inflation problems persist — no thanks to consumer resilience

This post was originally published on TKer.com

We’ve discussed how Fed-sponsored market beatings would continue until we got “clear and convincing” evidence that inflation was coming down.

We did not get that evidence last week.

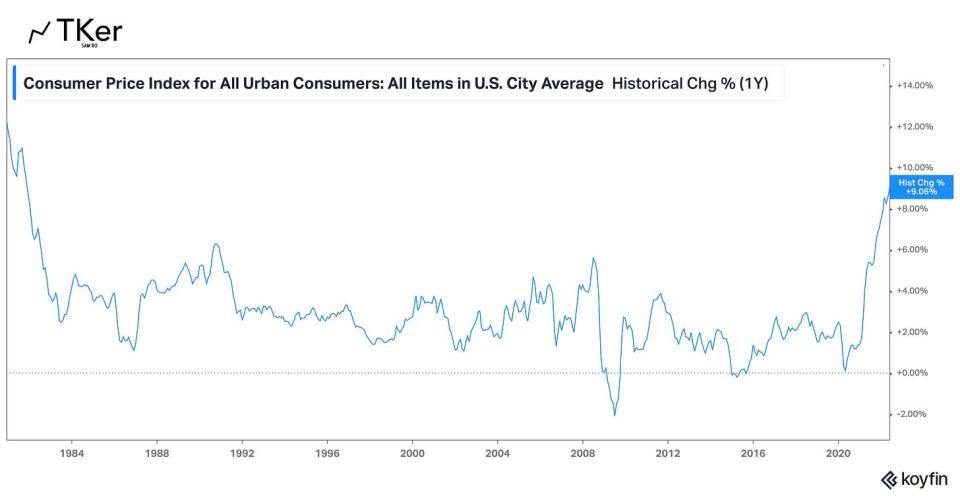

On Wednesday, we got a surprisingly hot consumer price index (CPI) report that followed last month’s surprisingly hot report.

In June, CPI jumped 1.3% month-over-month (highest since September 2005), driven by a 7.5% surge in energy prices that was underpinned by an 11.2% increase in gasoline prices.

CPI was up 9.1% on an annual basis, the biggest jump since November 1981. Energy prices were up 41.6% (highest since April 1980) and food prices were up 10.4% (highest since February 1981).

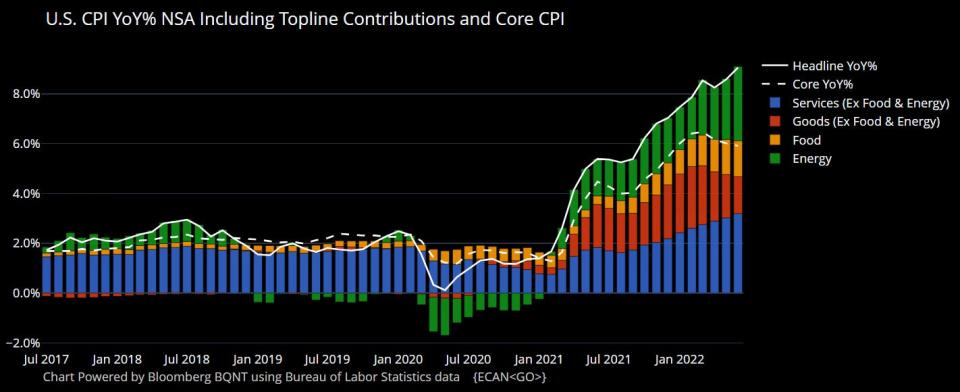

Excluding food and energy prices, which tend to be much more volatile in the short-run, core CPI accelerated to a hotter-than-expected 0.7%. This reflected a 5.9% gain from a year ago, which was below the peak of 6.4% print in March.

And while the annual increase in core CPI was off of its high, it was still high. The fact that the monthly rate is accelerating brought no comfort to anyone.

Core goods prices increased by 0.8% month-over-month and core services prices rose by 0.7%. The inflation was broad-based, with notable price gains for cars, clothes, and medical care. Hotel prices and airfares fell.

Michael McDonough, chief economist at Bloomberg, shared this great visualization breaking down what’s been driving CPI growth.

Shelter — a core service which accounts for a heavy 32% of CPI — was up 0.6% in June from a month ago. This includes rent of primary residence (a.k.a., tenants’ rent), which accelerated to 0.8% (highest since April 1986), and owners’ equivalent rent (i.e., how much a homeowner would have to pay to rent their currently owned home), which accelerated to 0.7% (highest since August 1990).

Bottom line: Inflation right now is about a lot more than volatile food and energy prices. The price for pretty much everything is inflating.

Sentiment remains in the dumps

Worries about inflation continue to keep consumer and business sentiment depressed.

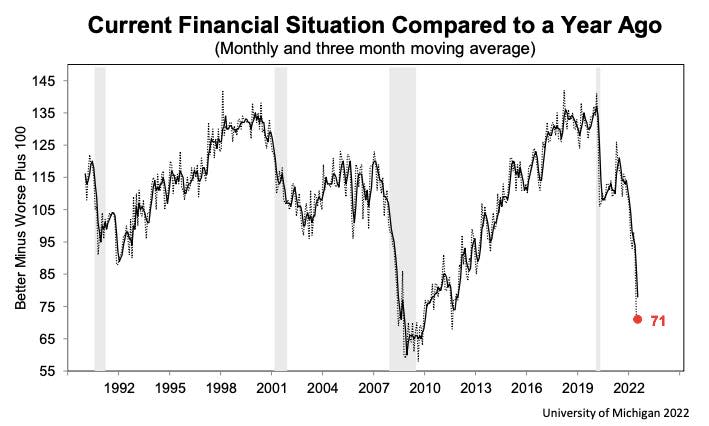

According to the University of Michigan’s July Survey of Consumer Sentiment released Friday, consumers are particularly gloomy about the state of their personal finances. From the survey’s director Joanne Hsu: “Current assessments of personal finances continued to deteriorate, reaching its lowest point since 2011… Consumers remained in agreement over the deleterious effect of prices on their personal finances. The share of consumers blaming inflation for eroding their living standards continued its rise to 49%, matching the all-time high reached during the Great Recession.“

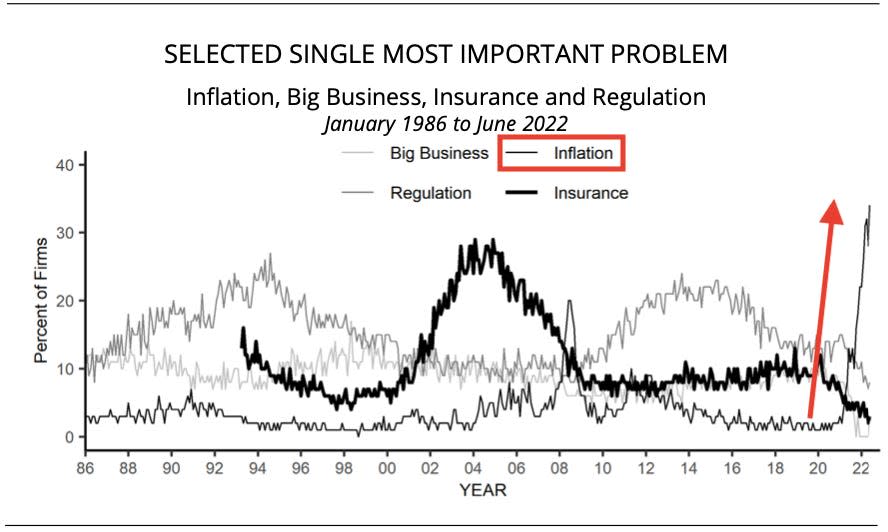

On Tuesday, the National Federation of Independent Business reported that its June small business Optimism Index fell to its lowest level since January 2013 as inflation concerns persisted. From the report: “Thirty-four percent of owners reported that inflation was their single most important problem in operating their business, an increase of 6 points from May and the highest level since 1980 Q4.“

And that said, consumers are paying up

Despite weak sentiment, consumers continue to spend at a healthy clip. (For more on this contradictory behavior, read this and this.)

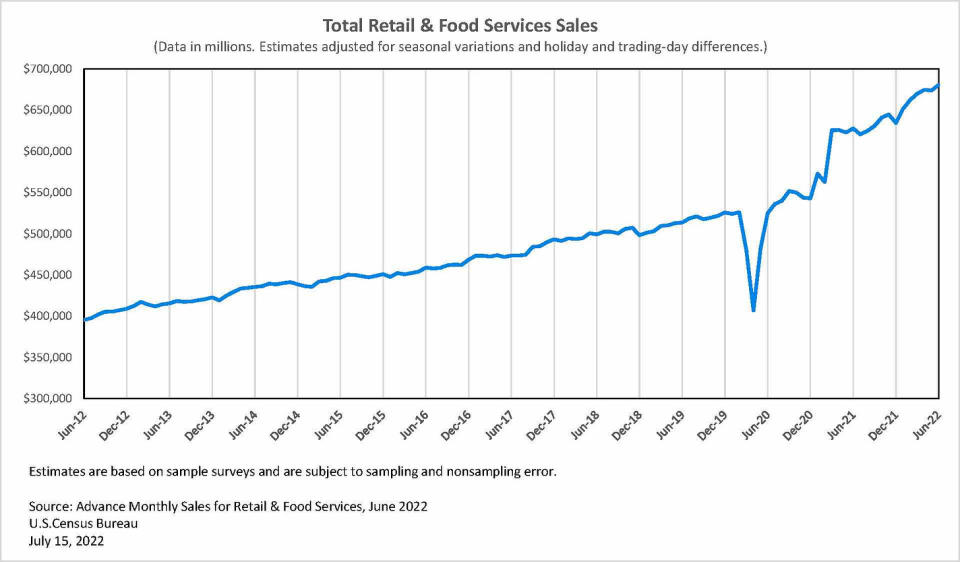

On Friday, we learned retail sales in June increased by a better-than-expected 1.0% from a month ago to a record $680.6 billion. Excluding automobile and gas prices — which tend to be volatile in the short term — sales jumped by a better-than-expected 0.7%.

Strength was broad-based with gains in most categories, including furniture, restaurants and bars, cars and parts, and electronics. While some goods categories declined, nothing was particularly weak.

The big banks confirmed that consumer spending had been resilient.

“We have yet to observe a pullback in discretionary spending, including in the lower income segments, with travel and dining growing a robust 34% year-on-year overall,“ Jeremy Barnum, CFO at JPMorgan Chase, said on the bank’s Q2 earnings call on Thursday.

But there’s one big caveat to all of this spending: inflation.

“We see the impact of inflation on higher nondiscretionary spend across income segments,” Barnum added. “Notably, the average consumer is spending 35% more year-on-year on gas and approximately 6% more on recurring bills and other nondiscretionary categories.“

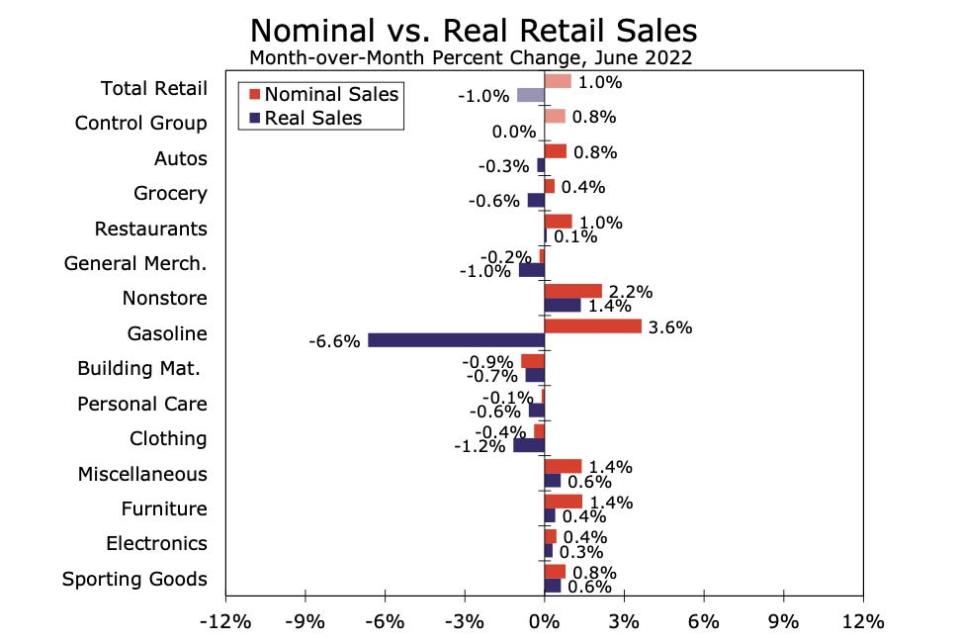

Indeed, June’s retail sales stats aren’t as robust when you adjust them for inflation.

“The June retail sales report shows that people are paying more but getting less,” Wells Fargo’s Tim Quinlan and Shannon Seery wrote on Friday. “After applying our inflation adjustment, we estimate that real retail sales actually fell by 1.0%.“

The economists charted how for most categories, sales fell when adjusted for the high inflation rate during the period.

Earning money to pay for inflation

What’s behind all of this consumer spending? Businesses that are hiring.

Earlier this month we learned U.S. employers added a whopping 372,000 jobs in June alone.

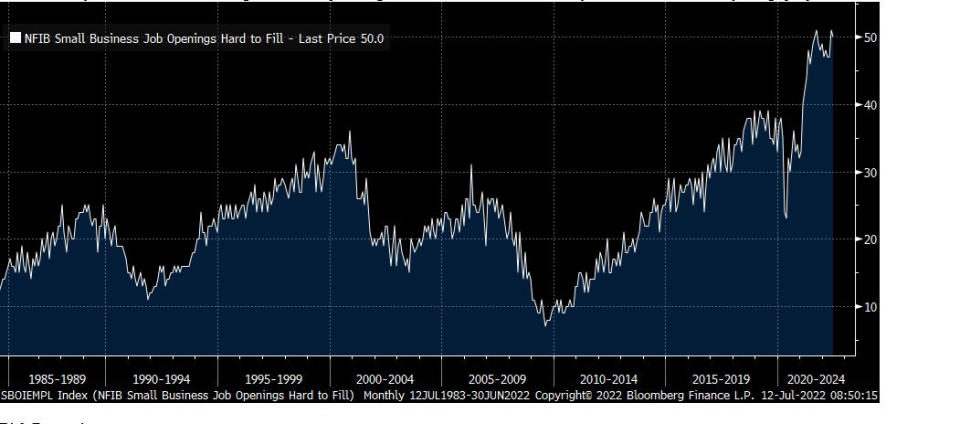

According to that gloomy NFIB sentiment survey we discussed earlier, a near-record level of employers said jobs were hard to fill. This confirms that most people who want jobs have jobs.

“If ‘we’re already in a recession,’ someone forgot to tell the super strong labor market,” tweeted Richard Bernstein Advisors in response to the NFIB data.

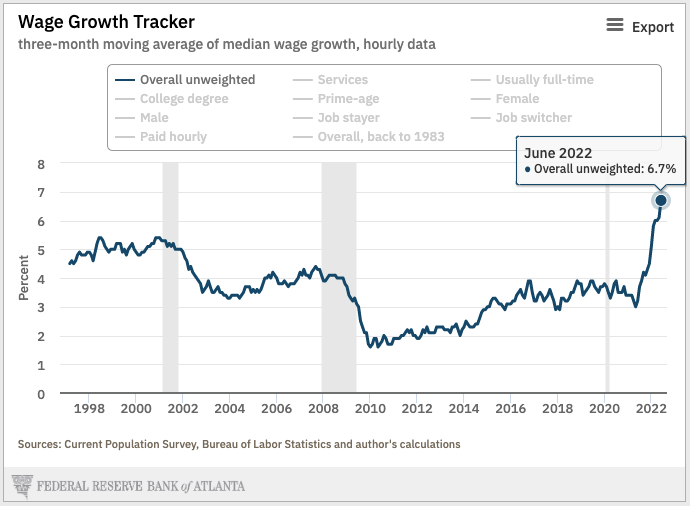

And these employers are paying up (which actually helps explain why business sentiment is poor).

According to the Atlanta Fed’s Wage Growth Tracker updated on Thursday, wage growth accelerated to 6.7% in June.1

Bottom line: Despite high prices and poor sentiment, job growth and rising wages have helped propel spending in the economy.

Good news continues to be bad news 🛑

Remember, good news in the economy is actually bad news right now if it’s the kind of thing that could push inflation higher.

The Fed is currently pummeling financial markets with tighter monetary policy to cool demand in the economy, which should ease demand for workers in this already tight labor market, which in turn should ease wage growth — which is bad in an economy with supply constraints because it enables businesses to raise prices because they know customers will pay. (For more on this, read this.)

While workers will be glad to hear about their higher pay and businesses should be happier about all that they’re able to sell, all of this is fueling the inflation that we’re continuing to experience. And high inflation is bad.

Now for some actual good news

One thing to remember about most economic reports is that much of it gets reported on a pretty significant lag.

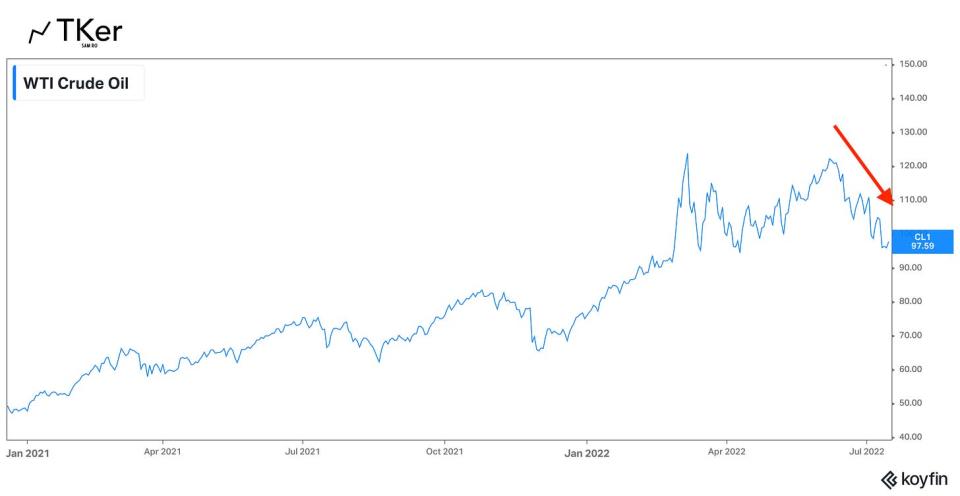

For example, data for the last week’s CPI report was gathered in June. But we’re halfway through July. And, we have real-time data for the price of oil: it’s been coming down since mid-June.

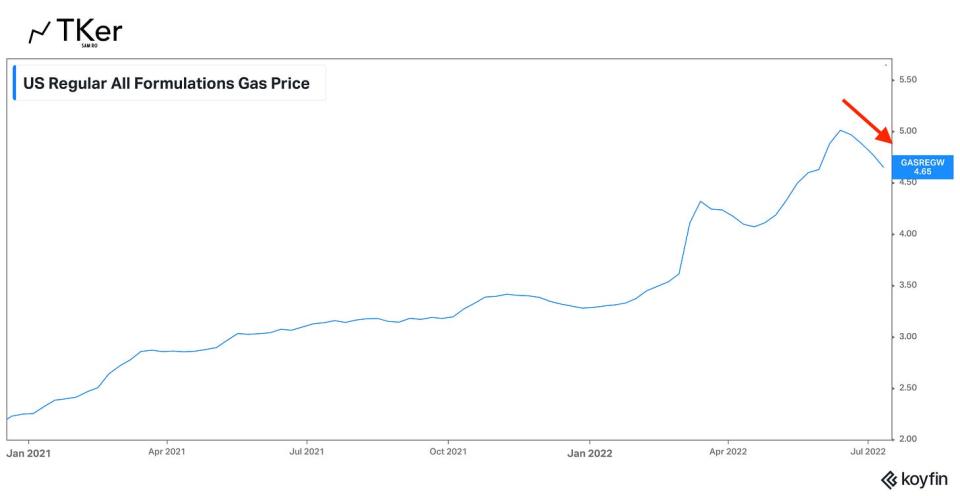

Same with gasoline prices, which have been coming down since mid-June. (The price of crude oil accounts for roughly 60% of the price of regular gasoline.)

This is important because energy prices factor into the costs of a lot of goods and services, which is one of the reasons why we have had high inflation.

Sure, the prices levels are still pretty high. But the point is that they are no longer going up at the moment. They’re coming down.

And it seems like consumers are catching on to some of these falling prices. The University of Michigan’s July Survey of Consumer Sentiment revealed that expectations for inflation one year from now decreased to 5.2% from 5.3% a month ago. Expectations for inflation five-to-ten years from now fell to 2.8% from 3.1%.

Yes, expectations are still high. And yes, this is just one month’s worth of data. But the direction is at least encouraging.

Some bad news that could be good news

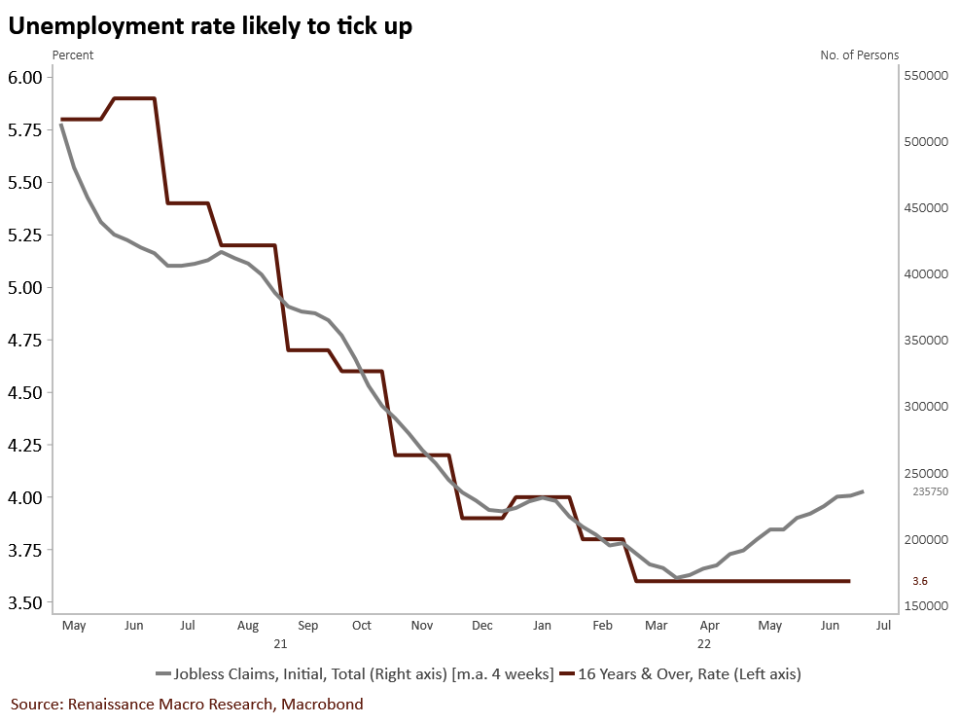

Another timely report is the Department of Labor’s weekly tally of unemployment insurance claims.

While the data continues to signal that the labor market is in pretty good shape, the trajectory of the numbers are starting to set off alarms.

Initial claims for unemployment insurance came in at 244,000 for the week ending July 9. The number is at a level that’s associated with economic expansions. But it’s up from its six-decade low of 166,000 in March and is now at its highest level since November 20.

“Initial claims running the highest level all year,“ Neil Dutta, head of U.S. economics at Renaissance Macro Research, said on Thursday. “Some rise in unemployment is inevitable at this point.”

This is unwelcome news for jobseekers. However, a cooling labor market should help ease wage growth, which in turn should cause inflation to come down. This is something the Fed is explicitly aiming for.

In other words, bad news in the labor market may be good news regarding inflation.

The big picture

Good news is bad news, and bad news is good news. Nominal numbers say one thing, but real numbers say something else. The Fed is trying to slow the economy, but it doesn’t intend to send the U.S. into a recession, but it also might be okay with a recession.

Understandably, this is all complicated.

Ultimately, everything in the economy and markets right now comes down to one problem: Inflation.

Inflation is high right now, and everyone agrees that persistently high inflation is bad for the economy. So the top priority right now is to bring inflation down. And policymakers like the Fed seem comfortable pushing the economy dangerously close to a recession if that’s what it takes. That’s because a recession now would be less bad than some inflation-fueled economic crisis down the road.

However, nobody wants a recession, especially if a recession doesn’t have to be a necessary condition of bringing inflation down. Indeed, even the Fed has explicitly said it does not intend to induce a recession.

And so you have a pair of economic narratives running parallel to each other that seem to be in conflict with each other: The inflation narrative, with hawks arguing that slow growth or a modest recession is necessary to bring prices down; And the economic growth narrative, with skeptics sounding the alarm on recession risks even though they understand that something has to be done to bring inflation down. They’re both saying the same thing — but from slightly different perspectives.

You also have a pair of market narratives running parallel to each other that also seem to be in conflict with each other: The shorter-term, “Don’t fight the Fed” crowd, who understand that Fed-sponsored market beatings will continue until inflation shows “clear and convincing” evidence that inflation is coming down; and the longer-term “Stocks usually go up” crowd who’ll argue that stocks are closer to a bottom than a top.2 They’re not exactly contradicting each other — but they sure sound like they are.

The bottom line: All of these confusing dynamics will persist as long as high inflation continues to force the Fed to actively rein in economic growth.

“In our view, it will take at least several consecutive monthly inflation readings of slowing price growth for the Federal Reserve to start to believe that it has the current inflation episode in check,“ Wells Fargo’s Sarah House wrote on Wednesday.

And so we wait.

-

Related from TKer:

5 critical questions corporate America will answer in the coming weeks 😥

My favorite visualization of short-term stock market performance 📊

The market beatings will continue until inflation improves 🥊

SPECIAL EDITION: The complicated mess of the markets and economy, explained 🧩

Last week 🪞

📉 Stocks fall: The S&P 500 fell 0.9% last week to close at 3,863.16. The index is now down 19.5% from its January 3 closing high of 4,796.56 and up 5.4% from its June 16 closing low of 3,666.77. For more on market volatility, read this and this. If you wanna read up on bear markets, read this and this.

As I wrote last month, it appears that the markets will be held hostage by the Fed as long as inflation isn’t showing “clear and convincing” signs of easing. Read more about this here and here.

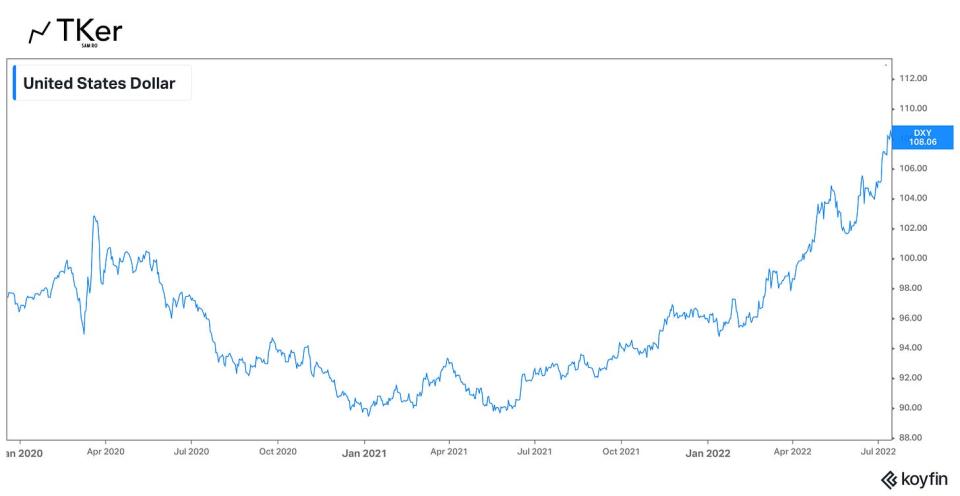

💸 Dollar strength: As the Fed has been tightening monetary policy, the resulting tighter financial conditions have come with a stronger dollar. The U.S. dollar index (DXY) — which tracks the value of the dollar relative to major world currencies — is up a whopping 13% year to date. At one point last week, the value of the euro fell to $1.

This is a headwind for U.S.-based multinational corporations. Read more about this here.

Next week 🛣

Earnings season picks up this week with Bank of America, Goldman Sachs, IBM, Johnson & Johnson, Netflix, Tesla, AT&T, and Verizon among the big companies to announce quarterly financial results.

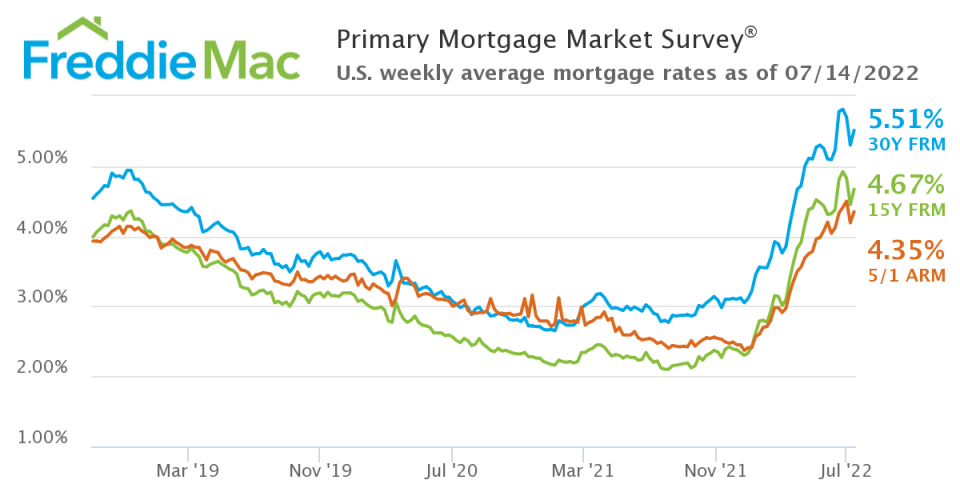

The week also comes with a lot of housing data with the July NAHB homebuilder sentiment index, the June housing starts report, and the June existing home sales report. High home prices and rising mortgage rates amid an economic slowdown are expected to hinder results.

1. The latest employment report from the Bureau of Labor Statistics (BLS) showed that wage growth decelerated in June, which is in conflict with the Atlanta Fed’s wage tracker. All of these reports come with a decent margin, and they employ varying methodologies in their calculations. That said, even with the deceleration in June, wage growth was still at a high level that would bolster a high inflation rate.

2. The S&P 500 is literally down 20% from its high.

This post was originally published on TKer.com

Sam Ro is the founder of Tk.co. Follow him on Twitter at @SamRo.

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

Download the Yahoo Finance app for Apple or Android

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube