Yahoo Finance

Yahoo Finance Is iLOOKABOUT's (CVE:ILA) 150% Share Price Increase Well Justified?

The most you can lose on any stock (assuming you don't use leverage) is 100% of your money. But if you buy shares in a really great company, you can more than double your money. For example, the iLOOKABOUT Corp. (CVE:ILA) share price has soared 150% in the last three years. How nice for those who held the stock! It's up an even more impressive 233% over the last quarter.

View our latest analysis for iLOOKABOUT

iLOOKABOUT isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually expect strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

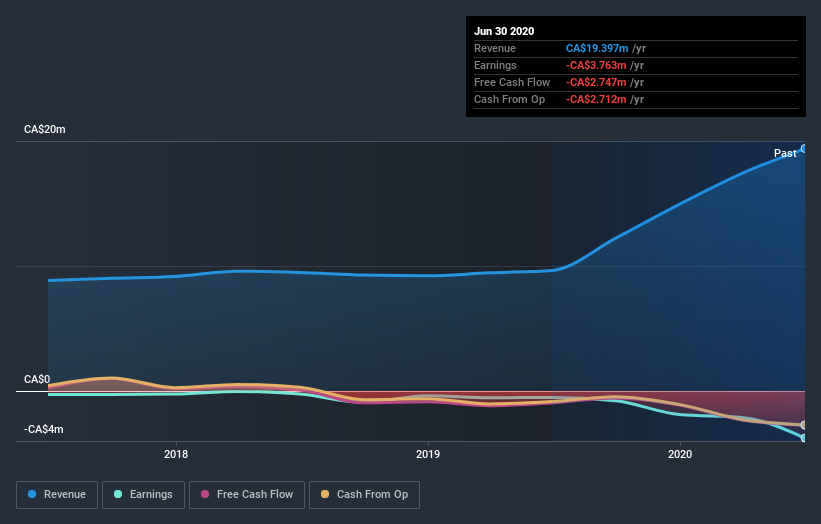

Over the last three years iLOOKABOUT has grown its revenue at 26% annually. That's well above most pre-profit companies. Along the way, the share price gained 36% per year, a solid pop by our standards. But it does seem like the market is paying attention to strong revenue growth. Nonetheless, we'd say iLOOKABOUT is still worth investigating - successful businesses can often keep growing for long periods.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. It might be well worthwhile taking a look at our free report on iLOOKABOUT's earnings, revenue and cash flow.

A Different Perspective

We're pleased to report that iLOOKABOUT shareholders have received a total shareholder return of 76% over one year. That's better than the annualised return of 8% over half a decade, implying that the company is doing better recently. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. It's always interesting to track share price performance over the longer term. But to understand iLOOKABOUT better, we need to consider many other factors. Take risks, for example - iLOOKABOUT has 4 warning signs (and 2 which don't sit too well with us) we think you should know about.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.