Yahoo Finance

Yahoo Finance Here's Why Investors Should Retain Thermo Fisher (TMO) Stock

Thermo Fisher Scientific Inc. (TMO) is gaining investors’ confidence, backed by the performance of the company’s end markets. Through the proven growth strategy powered by the PPI (Practical Process Improvement) Business System, Thermo Fisher continued to deliver differentiated performance in the first quarter.

Thermo Fisher’s clinical research business, PPD, also had a very strong start to the year, as it continues to benefit from revenue synergies. However, weak solvency and a competitive landscape are worrisome.

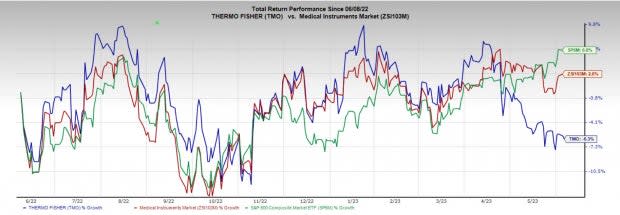

In the past year, this Zacks Rank #3 (Hold) stock has decreased 6.3% against the 2.6% rise of the industry and a 6% rise of the S&P 500 composite.

The renowned medical and laboratory equipment provider has a market capitalization of $200.03 billion. TMO has an earnings yield of 4.57% compared to the industry’s -7%. The company’s earnings surpassed estimates in all the trailing four quarters, delivering an average surprise of 5.99%.

Let’s delve deeper.

Upsides

Strong End Markets: Within the pharma and biotech end market, Thermo Fisher delivered growth in the mid-single digits in the first quarter. The company delivered a very strong performance in pharma services, clinical research and chromatography and mass spectrometry businesses.

Image Source: Zacks Investment Research

In academics and government, TMO witnessed growth across a range of its businesses, including biosciences, electron microscopy, chromatography and mass spectrometry, and the restructured safety market channel. Within industrial and applied, Thermo Fisher grew in the high single digits during the quarter, led by strong growth in all of its analytical instrument businesses, including electron microscopy, chromatography and mass spectrometry.

Growth Strategy Looks Promising: Starting with the first pillar, innovation, the company launched many high-impact new products across businesses in the first quarter. These include the Thermo Scientific iCAP RQ Plus ICP-MS Analyzer, the Applied Biosystems QuantStudio Absolute Q AutoRun dPCR Suite and the Invitrogen DynaGreen.

For the second pillar, TMO continues to strengthen its capabilities to serve emerging markets by opening a new Gibco cell culture rapid prototyping facility at the existing site in Suzhou, China. This facility will help regional customers accelerate the transition of their cell culture media production into current good manufacturing practices.

For the third pillar, Thermo Fisher achieved an exciting milestone in its strategic partnership with the University of California, San Francisco. In the first quarter, TMO announced the opening of a new cell therapy cGMP Manufacturing and Collaboration Center, to accelerate the development of breakthrough therapies for glioblastoma, multiple myeloma and other cancers.

PPD Acquisition Seems Strategic: In December 2021, Thermo Fisher completed its colossal $17.4-billion acquisition of PPD, Inc., a renowned global contract research organization providing clinical research services to the biopharma and biotech industry. The acquisition is anticipated to expand Thermo Fishers’ global reach in the attractive, high-growth clinical research services industry.

On the first-quarter earnings update, the company noted that PPD business growth continued to be in the mid-teens. Thermo Fisher had a strong backlog and a good level of authorization, which will continue to benefit the company from revenue synergies.

Downsides

Tough Competitive Pressure: For its diversified portfolio, Thermo Fisher faces different types of competitors, including a broad range of manufacturers and third-party distributors. The competitive landscape is quite tough with changing technology and customer demands that require continuous research and development.

Weak Solvency: At the quarter-end, TMO had approximately $35.3 billion of total debt, much higher than the corresponding cash and cash equivalent level of $3.48 billion. The times interest earned for the company stands at 8.5%, suggesting a sequential decline from 11.8% at the end of the fourth quarter.

Estimate Trend

Thermo Fisher has been witnessing a negative estimate revision trend for 2023. The Zacks Consensus Estimate for 2023 earnings per share (EPS) has moved from $23.70 to $23.69 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $45.31 billion. This suggests a 0.9% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Zimmer Biomet ZBH, Penumbra PEN and Hologic, Inc. HOLX.

Zimmer Biomet has an earnings yield of 5.71% compared to the industry’s -2.36%. Zimmer Biomet’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 7.38%. Its shares have increased 10.8% against the industry’s 30% decline in the past year.

ZBH sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Penumbra, sporting a Zacks Rank #1 at present, has an estimated growth rate of 64.1% for 2024. Penumbra shares have risen 129.4% compared with the industry’s 2.6% increase over the past year.

PEN’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 109.4%.

Hologic, carrying a Zacks Rank #2 (Buy) at present, has an earnings yield of 4.92% compared to the industry’s -7%. Shares of HOLX have risen 4.5% compared with the industry’s 2.6% growth over the past year.

Hologic’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 27.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Thermo Fisher Scientific Inc. (TMO) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Zimmer Biomet Holdings, Inc. (ZBH) : Free Stock Analysis Report

Penumbra, Inc. (PEN) : Free Stock Analysis Report