Yahoo Finance

Yahoo Finance Here's Why BATM Advanced Communications (LON:BVC) Can Manage Its Debt Responsibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, BATM Advanced Communications Ltd. (LON:BVC) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for BATM Advanced Communications

How Much Debt Does BATM Advanced Communications Carry?

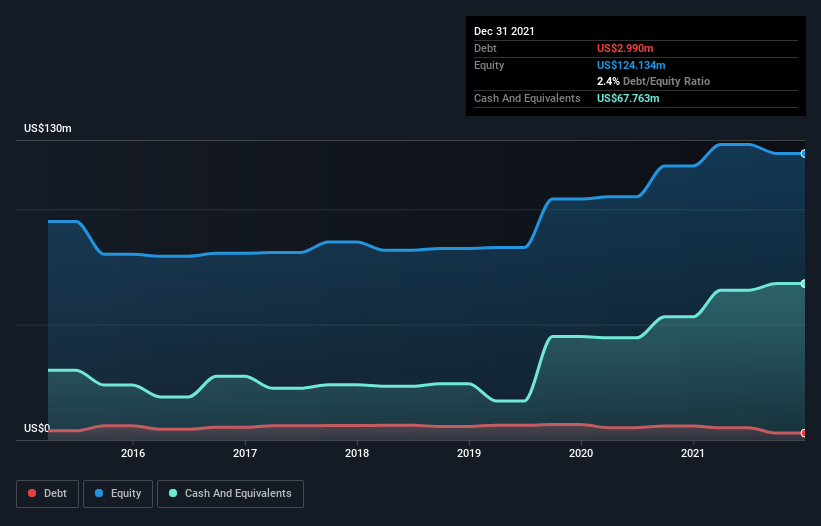

As you can see below, BATM Advanced Communications had US$2.99m of debt at December 2021, down from US$6.04m a year prior. But on the other hand it also has US$67.8m in cash, leading to a US$64.8m net cash position.

How Healthy Is BATM Advanced Communications' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that BATM Advanced Communications had liabilities of US$57.9m due within 12 months and liabilities of US$11.1m due beyond that. Offsetting this, it had US$67.8m in cash and US$34.9m in receivables that were due within 12 months. So it actually has US$33.7m more liquid assets than total liabilities.

This surplus suggests that BATM Advanced Communications has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that BATM Advanced Communications has more cash than debt is arguably a good indication that it can manage its debt safely.

But the bad news is that BATM Advanced Communications has seen its EBIT plunge 17% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if BATM Advanced Communications can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While BATM Advanced Communications has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last two years, BATM Advanced Communications produced sturdy free cash flow equating to 68% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that BATM Advanced Communications has net cash of US$64.8m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of US$2.3m, being 68% of its EBIT. So we don't have any problem with BATM Advanced Communications's use of debt. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with BATM Advanced Communications , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.