Yahoo Finance

Yahoo Finance If You Had Bought Siyata Mobile (CVE:SIM) Stock A Year Ago, You'd Be Sitting On A 33% Loss, Today

Investors can approximate the average market return by buying an index fund. When you buy individual stocks, you can make higher profits, but you also face the risk of under-performance. Investors in Siyata Mobile Inc. (CVE:SIM) have tasted that bitter downside in the last year, as the share price dropped 33%. That falls noticeably short of the market return of around 12%. On the bright side, the stock is actually up 12% in the last three years. The falls have accelerated recently, with the share price down 26% in the last three months. We note that the company has reported results fairly recently; and the market is hardly delighted. You can check out the latest numbers in our company report.

See our latest analysis for Siyata Mobile

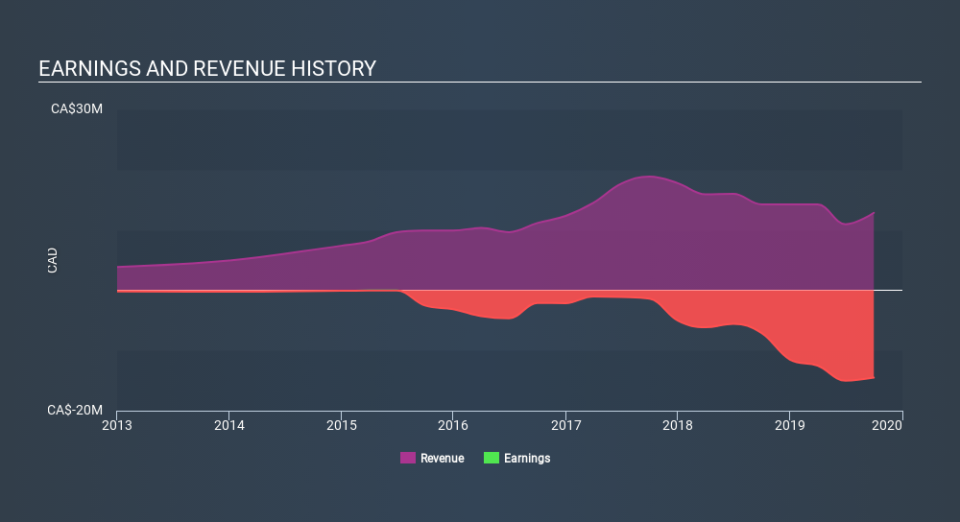

Given that Siyata Mobile didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually expect strong revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In just one year Siyata Mobile saw its revenue fall by 9.7%. That looks pretty grim, at a glance. The stock price has languished lately, falling 33% in a year. That seems pretty reasonable given the lack of both profits and revenue growth. It's hard to escape the conclusion that buyers must envision either growth down the track, cost cutting, or both.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

A Different Perspective

Siyata Mobile shareholders are down 33% for the year, but the broader market is up 12%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Fortunately the longer term story is brighter, with total returns averaging about 3.7% per year over three years. Sometimes when a good quality long term winner has a weak period, it's turns out to be an opportunity, but you really need to be sure that the quality is there. Before spending more time on Siyata Mobile it might be wise to click here to see if insiders have been buying or selling shares.

We will like Siyata Mobile better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.