Yahoo Finance

Yahoo Finance If You Had Bought Mene (CVE:MENE) Stock A Year Ago, You Could Pocket A 97% Gain Today

If you want to compound wealth in the stock market, you can do so by buying an index fund. But you can significantly boost your returns by picking above-average stocks. To wit, the Mene Inc. (CVE:MENE) share price is 97% higher than it was a year ago, much better than the market return of around 35% (not including dividends) in the same period. If it can keep that out-performance up over the long term, investors will do very well! Mene hasn't been listed for long, so it's still not clear if it is a long term winner.

See our latest analysis for Mene

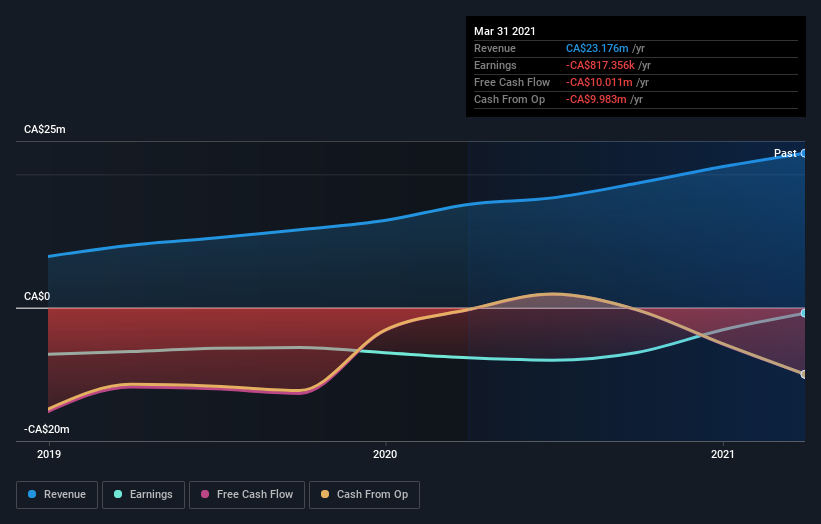

Given that Mene didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

Over the last twelve months, Mene's revenue grew by 50%. That's stonking growth even when compared to other loss-making stocks. While the share price gain of 97% over twelve months is pretty tasty, you might argue it doesn't fully reflect the strong revenue growth. If that's the case, now might be the time to take a close look at Mene. Human beings have trouble conceptualizing (and valuing) exponential growth. Is that what we're seeing here?

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Take a more thorough look at Mene's financial health with this free report on its balance sheet.

A Different Perspective

Mene boasts a total shareholder return of 97% for the last year. A substantial portion of that gain has come in the last three months, with the stock up 27% in that time. Demand for the stock from multiple parties is pushing the price higher; it could be that word is getting out about its virtues as a business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Like risks, for instance. Every company has them, and we've spotted 3 warning signs for Mene (of which 1 is potentially serious!) you should know about.

We will like Mene better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.