Yahoo Finance

Yahoo Finance Gold Bull Market To Resume In 2022

The widespread scepticism towards gold among the investment community likely provides an excellent opportunity to buy the metal as the fundamental backdrop continues to improve. The metal has registered a series of higher lows and appears to be consolidating ahead of a resumption of its multi-year bull market.

Fundamentals Continue To Improve

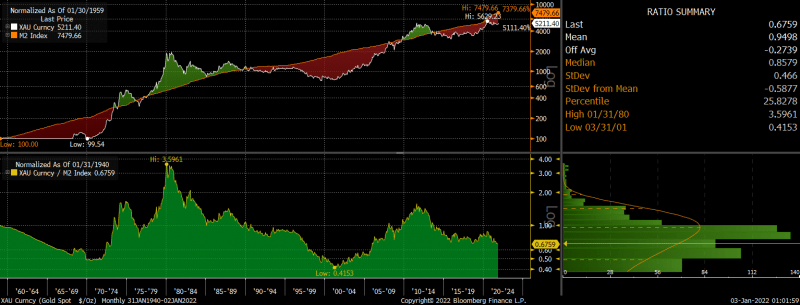

Over the long term, the price of gold tends to be driven by the supply of money in the economy, and the 40% increase in M2 over the past two years is highly positive for the metal. While there have been huge swings in the ratio of gold to the money supply in the past, periods when the ratio has been depressed as it is now have resulted in subsequent outperformance over a multi-year period.

Ratio of Gold over M2

Over the shorter term, the price of gold tends to be driven by changes in real interest rate expectations. Such expectations are best captured by the yield on 10-year investment-linked bonds, which are effectively the bond market’s expectations of the difference between interest rates and inflation. When inflation expectations rise faster than interest rate expectations, the opportunity cost of holding gold declines, lifting its price. This can be seen in the chart below.

Gold vs 10-Year Inflation-Linked Bond Yield (Inverted)

What is noteworthy is that despite the rise in nominal bond yields seen in 2021, the rise in inflation expectations has seen real bond yields continue to decline. If the correlation between gold and real bond yields remains intact, as I believe it should, then gold should be trading around the USD2000/oz level.

Of course, the correlation could remain intact by real bond yields rising, which cannot be ruled out. However, the risks seem heavily weighted to the downside. The main reason is that 10-year inflation expectations remain at just 2.6%, which is fully 430 basis points below the trailing inflation rate. As it becomes increasingly clear that above-average inflation rates are here to stay, I expect this to become reflected in real bond yields and the price of gold. As for the potential for the Fed to hike interest rates aggressively, such a scenario seems highly unlikely in the context of record debt ratios at the corporate and government level.

Headline CPI vs 10-Year Breakeven Inflation Expectations, %

Source: Bloomberg

Price Action Improving

The continued improvement in gold’s fundamentals is at last being matched by an improvement in the technical picture. The metal has posted a series of higher lows since bottoming in March 2021, and from a longer-term perspective a bullish pennant appears to have formed, suggesting an upside break over the coming months. Time will tell, but from a risk reward perspective, gold looks like a great buy here.

Gold Price, USD/oz

This article was originally posted on FX Empire