Yahoo Finance

Yahoo Finance If You Like EPS Growth Then Check Out TC Energy (TSE:TRP) Before It's Too Late

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

In contrast to all that, I prefer to spend time on companies like TC Energy (TSE:TRP), which has not only revenues, but also profits. While profit is not necessarily a social good, it's easy to admire a business than can consistently produce it. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Check out our latest analysis for TC Energy

How Fast Is TC Energy Growing Its Earnings Per Share?

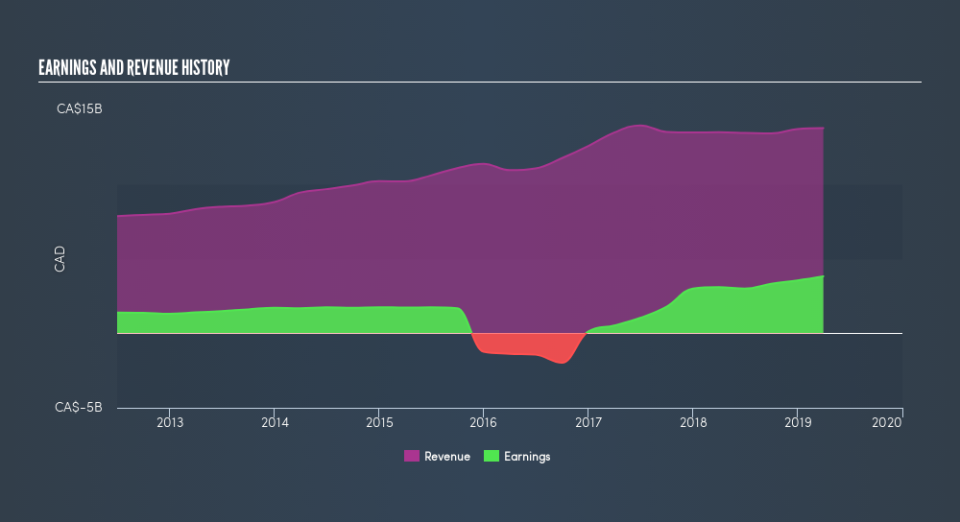

In the last three years TC Energy's earnings per share took off like a rocket; fast, and from a low base. So the actual rate of growth doesn't tell us much. Thus, it makes sense to focus on more recent growth rates, instead. TC Energy boosted its trailing twelve month EPS from CA$3.52 to CA$4.18, in the last year. That's a 19% gain; respectable growth in the broader scheme of things.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. TC Energy shareholders can take confidence from the fact that EBIT margins are up from 34% to 43%, and revenue is growing. That's great to see, on both counts.

In the chart below, you can see how the company has grown earnings, and revenue, over time. Click on the chart to see the exact numbers.

While we live in the present moment at all times, there's no doubt in my mind that the future matters more than the past. So why not check this interactive chart depicting future EPS estimates, for TC Energy?

Are TC Energy Insiders Aligned With All Shareholders?

Like that fresh smell in the air when the rains are coming, insider buying fills me with optimistic anticipation. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Although we did see some insider selling (worth -CA$1.2m) this was overshadowed by a mountain of buying, totalling CA$2.5m in just one year. This makes me even more interested in TC Energy because it suggests that those who understand the company best, are optimistic. We also note that it was the Executive VP & President of U.S. Natural Gas Pipelines, Stanley Chapman, who made the biggest single acquisition, paying CA$557k for shares at about CA$44.89 each.

Along with the insider buying, another encouraging sign for TC Energy is that insiders, as a group, have a considerable shareholding. Indeed, they hold CA$57m worth of its stock. That's a lot of money, and no small incentive to work hard. Even though that's only about 0.09% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

Does TC Energy Deserve A Spot On Your Watchlist?

One important encouraging feature of TC Energy is that it is growing profits. On top of that, we've seen insiders buying shares even though they already own plenty. To me, that all makes it well worth a spot on your watchlist, as well as continuing research. Of course, just because TC Energy is growing does not mean it is undervalued. If you're wondering about the valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of TC Energy, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.