Yahoo Finance

Yahoo Finance Kevin Carmichael: Economy grows faster than expected, raising odds of another big rate hike

Economic growth in the third quarter was much faster than the Bank of Canada predicted, raising the odds of another outsized interest rate increase before year’s end to quiet inflation.

Normally, evidence of surprisingly strong growth would be welcome news. That’s less true today, because the Bank of Canada is desperately trying to contain the fastest inflation since the 1980s by ratcheting up the cost of borrowing.

Governor Tiff Macklem has raised the benchmark rate by 3.5 percentage points since March in a bid to suffocate inflation that peaked at about eight per cent over the summer, and continues to hover around seven per cent, well above what anyone defines as sustainable.

That means economic growth needs to slow, because current demand far exceeds the ability of Canada’s companies to keep up with orders. Price pressures will remain intense until supply and demand rebalance, robbing companies of the ability to charge more for goods and services.

“The economy is still in excess demand — it is overheated,” Macklem told the House finance committee last week.

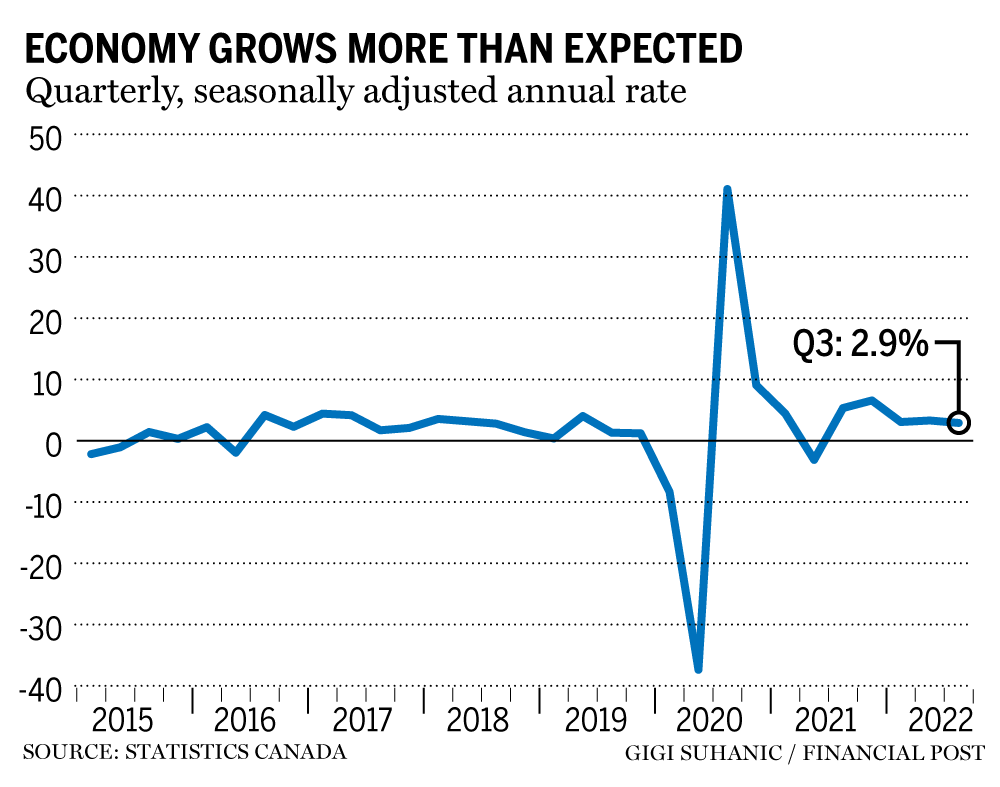

That’s why Macklem probably will dislike Statistics Canada’s latest tally of gross domestic product. The agency on Nov. 29 reported that GDP grew at an annual rate of 2.9 per cent in the July-to-September period, slower than the previous quarter, but considerably stronger than the 1.5 per cent pace the Bank of Canada foresaw in its latest economic outlook.

The results suggest the economy was having little trouble pushing through the headwinds from the Bank of Canada’s unusually aggressive approach to interest rate increases, highlighted by a full percentage point hike in July.

The central bank, which was caught flat-footed as inflation surged in the aftermath of the COVID-19 recession, has now resorted to outsized changes to the policy rate as it attempts to catch up to inflation that has surged far ahead of its two per cent target for year-over-year increases in the consumer price index.

Macklem’s latest move was a half-point increase on Oct. 26, at which time he indicated that borrowing costs were getting close to hitting a ceiling, but weren’t there yet. The comment caused Bay Street analysts to start debating the “terminal rate,” which most think is probably around 4.25 per cent, and whether the Bank of Canada might continue to taper its increases heading into 2023.

The GDP numbers likely tilt the argument in favour of those who think the Bank of Canada will go with another half-point increase when policymakers next update policy on Dec. 7. “There’s nothing here to keep the Bank of Canada from hiking rates (a half-point) at the December policy announcement,” Benjamin Reitzes, an economist at Bank of Montreal, said in a note to his clients.

Demand clearly remains stronger than the Bank of Canada presumed in October

Veronica Clark, economist, Citigroup Global Markets

Exports, investment in non-residential structures and stockpiling by companies led the increase, Statistics Canada said. Growth in those corners of the economy was partially offset by drops in housing investment and consumer spending, both of which would be the first to suffer from higher borrowing costs and inflation’s burden on the cost of living.

The housing and consumer spending data might be sending a truer signal about the state of the economy than the headline GDP number, which was flattered by surging prices for Canadian exports of oil, natural gas and farm commodities such as wheat.

Exports have a bigger sway over Canada’s economy than other advanced economies, but household consumption still represents about 56 per cent of GDP. Consumer demand declined at an annual rate of one per cent in the third quarter, after surging 9.5 per cent in the second quarter, as demand for goods such as new trucks and furniture receded. It was the first drop since the second quarter of 2021.

The household savings rate increased to 5.7 per cent from 5.1 per cent in the second quarter, suggesting consumers might be hunkering down for the recession that many forecasters say is inevitable. Meanwhile, investment in residential structures dropped for a second consecutive quarter, reflecting reduced demand amid higher mortgage rates.

FP Answers: Why is the Bank of Canada losing money and does it matter?

Alberta forecasts smaller surplus as Danielle Smith opts to spend some of the oil windfall

Separately, Statistics Canada said GDP — measured by industrial output — increased 0.1 per cent in September from the previous month, compared with a 0.3 per cent gain in August. The agency said preliminary data suggest economic output was unchanged in October, implying the economy was losing momentum quickly as summer turned to fall, and suggesting the Bank of Canada’s interest rate increases will bite in the fourth quarter.

“There are worrying trends under the headline,” James Orlando, an economist at Toronto-Dominion Bank, said in a note to clients. “Rising interest rates and high inflation have weighed on consumer spending, a trend which has started earlier than expected, but should last through the year.”

Damping households’ impulse to spend is the plan. Macklem has repeatedly said the central bank will do everything in its analytical power to avoid causing a recession, but has left little doubt he intends to err on the side of doing whatever it takes to snuff out inflation, which he sees as a more serious long-term threat to the economy than a downturn of short duration.

The Bank of Canada’s forecast predicts fourth-quarter growth at an annual rate of 0.5 per cent, which means policymakers think the economy will have to stall over the next few months to get inflation back to two per cent. The economy entered the fourth quarter with more momentum than that forecast anticipated, suggesting policymakers will feel compelled to hit the brakes that much harder when they decide interest rates next week.

“Demand clearly remains stronger than the Bank of Canada presumed in October,” Veronica Clark, an economist at Citigroup Global Markets Inc., said in a note.

• Email: kcarmichael@postmedia.com | Twitter: carmichaelkevin