Yahoo Finance

Yahoo Finance Diageo (DEO) 1H FY23 Earnings & Sales Rise on Strong Demand

Diageo plc DEO reported interim results for the first half of fiscal 2023, ended Dec 31, 2022, wherein pre-exceptional earnings per share improved 15.2% year over year to 98.6 pence (in local currency). This was backed by robust sales growth, organic operating margin expansion, productivity savings and favorable currency impact.

Although the company predicts a challenging operating environment for fiscal 2023, it remains confident of the resilience of its business and its ability to navigate through these headwinds. The company is confident about the long-term growth potential of the total beverage alcohol sector and expects to expand its value share by 50% in the sector to 6% by 2030.

The company notes that it is on track to deliver on its medium-term guidance for fiscal 2023-2025, wherein it targets organic sales growth of 5-7% and organic operating profit growth of 6-9%.

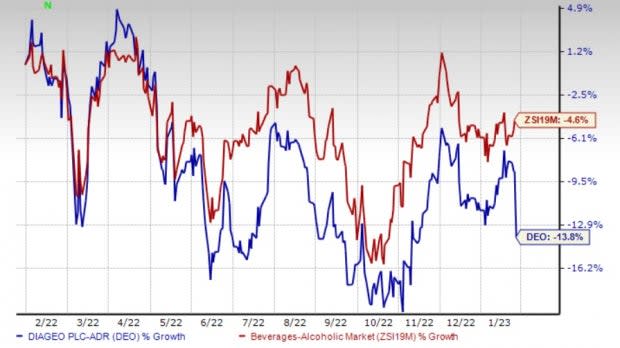

Shares of the Zacks Rank #3 (Hold) company have declined 13.8% in the past year compared with the industry’s fall of 4.6%.

Image Source: Zacks Investment Research

1H FY23 Highlights

On a reported basis, net sales increased 18.4% year over year, driven by strong organic growth and favorable currency effects. Organic net sales were up 9.4% year over year due to growth across all regions. The company’s diversified footprint, advantaged portfolio, strong brands and favorable industry trends of premiumization aided top-line growth.

Organic volume improved 1.8% year over year. Price/mix grew 7.6% year over year, reflecting a high-single-digit price contribution to net sales growth. The company’s premium plus brands contributed 57% to net sales growth and 65% to organic sales growth. Its super-premium-plus brands aided organic net sales by 12%.

In North America, Diageo’s largest market, sales accelerated 19% year over year on organic sales growth of 3% and strength across all markets. On a year-over year basis, DEO witnessed sales growth of 13% in Europe, 20% in the Asia Pacific, 9% in Africa and 34% in Latin America and the Caribbean.

Strong growth in Europe was driven by organic growth of 10% and the hyperinflation adjustments related to Turkey. Sales in the Asia-Pacific reflected gains from strength across most markets, notably South East Asia, Travel Retail Asia and the Middle East and India. Growth across all markets, supported by price increases, aided sales growth in Africa. Latin America and the Caribbean sales growth reflected gains in Brazil, Central America, and the Caribbean and Mexico, mainly on price increases and premiumization.

On a year-over year basis, Diageo also reported substantial growth across most categories, with growth of 28% slated for tequila, 19% for scotch, 10% for Spirits, 5% for Rum, 9% for beer and 8% for ready-to-drink. However, Vodka sales declined 2%. Gains in the beer business were driven by growth across all regions and double-digit growth of Guinness in Ireland, Great Britain and North America.

The reported operating profit improved 15.2% year over year due to an improved organic operating profit and the positive impact of currency rates. The reported operating margin declined 92 basis points (bps) as the aforementioned gains were more than offset by exceptional operating items, acquisitions and disposals and other items.

Organic operating profit rose 9.7% year over year, with the organic operating margin expanding 9 bps. Organic operating profit benefited from leverage in operating costs, driven by disciplined cost management, despite inflation. Moreover, growth was driven by supply productivity savings and price increases, which more than offset the higher cost inflation on the gross margin. Organic operating margin also reflected strong operating margin expansion in the Asia Pacific and Europe, partially offset by a decline in North America.

Financials

In the first half of fiscal 2023, Diageo delivered net cash from operating activities of £1,248 million, marking a decline of £699 million year over year. DEO reported strong free cash flow of £817 million, down £758 million from the last-year level due to strong working capital outflow, higher cash tax and interest, as well as increased capital investments.

Diageo is committed to its disciplined approach to capital allocation, primarily to enhance its shareholder value. DEO increased the interim dividend 5% to 30.83 pence per share. This reflects its strong liquidity position and confidence in the long-term health of its business.

Additionally, Diageo expects to complete the remaining £0.3 billion of share repurchases as part of the return of capital program of up to £4.5 billion in February 2023. Further, it expects incremental share buybacks of £0.5 billion in fiscal 2023.

For fiscal 2023, the company expects capital expenditure of £1-£1.2 billion. Moreover, it expects to report strong free cash flow in the second half of fiscal 2023 compared with the first half due to the lapping of more normalized working capital outflows witnessed in the second half of fiscal 2022.

Fiscal 2023 Outlook

In North America, the company expects organic net sales growth to normalize through the second half of fiscal 2023 compared to double-digit growth in the year-ago period. In Europe, organic net sales growth is likely to moderate in the second half of fiscal 2023 as the company’s laps the on-trade channel re-opening and recovery in the prior year. The company anticipates continued organic net sales growth for the Asia Pacific, Latin America and the Caribbean and Africa in the second half of fiscal 2023, although at a moderated pace relative to strong growth in fiscal 2022.

The company expects to continue its revenue management initiatives, including pricing actions, throughout fiscal 2023, to overcome the challenging inflationary environment. It expects marketing investment to increase more than sales growth in the second half of fiscal 2023. The company anticipates the organic operating margin to benefit from continued premiumization trends, everyday efficiencies and operating expense leverage, offset by strong investments in marketing.

The company estimates the tax rate before pre-exceptional items to be 22-24% in fiscal 2023. The effective interest rate is likely to be 4% in fiscal 2023.

Looking for Solid Stocks? Check These

We highlighted three better-ranked companies in the Consumer Staples sector, namely Anheuser-Busch InBev BUD, The Coca-Cola Company KO and Monster Beverage MNST.

Anheuser-Busch InBev, alias AB InBev, is a global brewing company with more than 500 iconic brands. It presently carries a Zacks Rank #2 (Buy). BUD has an expected EPS growth rate of 9.7% for three to five years. The BUD stock has declined 5.1% in the past year.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for AB InBev’s sales and EPS for the current financial year suggests growth of 7.3% and 2.8%, respectively, from the year-ago levels. BUD has a trailing four-quarter earnings surprise of 8.8%, on average.

Coca-Cola, a global beverage giant, presently has a Zacks Rank of 2. KO has a trailing four-quarter earnings surprise of 8.8%, on average. Shares of KO have declined 0.1% in the past year.

The Zacks Consensus Estimate for Coca-Cola’s sales and EPS for the current financial year suggests respective growth of 10.8% and 6.9% from the year-ago period’s reported figures. KO has an expected EPS growth rate of 6.2% for three to five years.

Monster Beverage, a marketer and distributor of energy drinks and alternative beverages, presently has a Zacks Rank #2. MNST has an expected EPS growth rate of 11.4% for three to five years. Shares of MNST have rallied 21.8% in the past year.

The Zacks Consensus Estimate for Monster Beverage’s sales for the current financial year suggests growth of 15.2% from the year-ago period’s reported figure. MNST has a negative earnings surprise of 7.5% in the trailing four quarters, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CocaCola Company (The) (KO) : Free Stock Analysis Report

Diageo plc (DEO) : Free Stock Analysis Report

Anheuser-Busch InBev SA/NV (BUD) : Free Stock Analysis Report

Monster Beverage Corporation (MNST) : Free Stock Analysis Report