Yahoo Finance

Yahoo Finance The Crash is an Opportunity for Snap Inc.'s (NYSE: SNAP) Insiders to Start Buying

This article first appeared on Simply Wall St News.

If a corporate boogeyman existed, explicitly designed to haunt the tech platforms reliant on advertisement revenues, it would be called "Policy Changes."

Although Apple's iOS 14.5 update announced tracking transparency months ago, it took some time for its aftershock to hit the environment, as companies like Snap Inc. (NYSE: SNAP) saw the impact on the revenues.

See our latest analysis for Snap.

Third-quarter 2021 results:

• Revenue: US$1.07b (up 57% from 3Q 2020).

• Net loss: US$72.0m (loss narrowed 64% from 3Q 2020).

Over the last 3 years, on average, earnings per share have increased by 24% per year, but its share price has risen by 106% per year, which means it is tracking significantly ahead of earnings growth.

However, the company missed the lower end of guidance, as the CEO Evan Spiegel blamed multiple factors – changes in advertising trackings and macroeconomic factors impacting their revenue partners. While many companies face labor shortages and supply-chain issues, pressuring the short-term marketing efforts, it is necessary to reflect on why Snap is so susceptible to these changes.

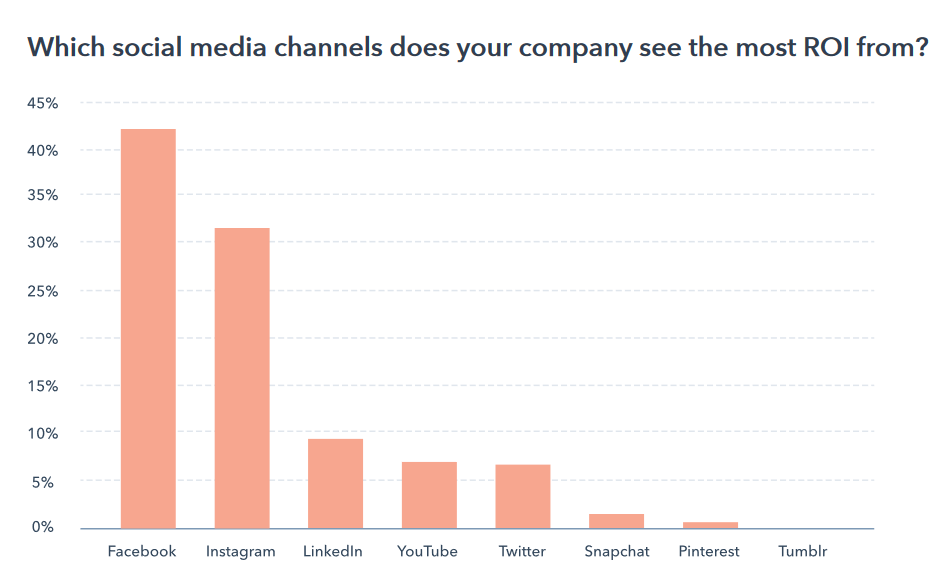

Observing the data compiled by Hubspot, it is evident that the clients' ROI is significantly lagging behind the competition.

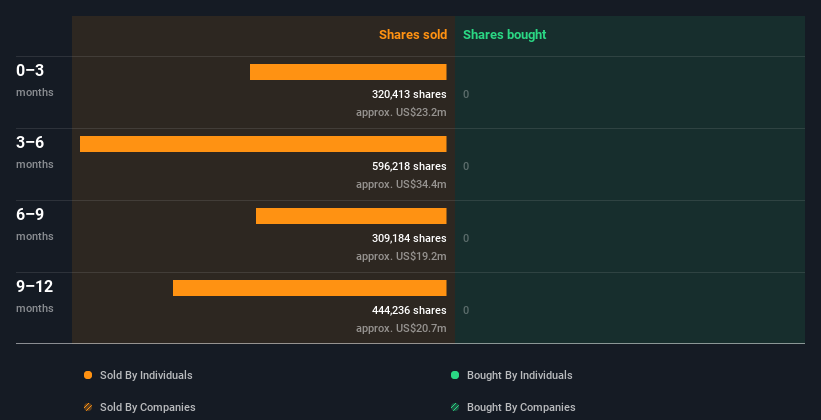

Snap Insider Transactions Over The Last Year

The Co-Founder, Evan Spiegel, made the biggest insider sale in the last 12 months. That single transaction was for US$19m worth of shares for US$67.81 each. While insider selling is negative, it is more negative if the shares are sold at a lower price. The good news is that this large sale was well above the current price of US$55.14. So it may not tell us anything about how insiders feel about the current share price.

Insiders in Snap didn't buy any shares in the last year. You can see the insider transactions (companies and individuals) over the previous year depicted in the chart below. If you click on the chart, you can see all the individual transactions, including the share price, individual, and date!

I will like Snap better if I see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Snap Insiders Are Selling The Stock

The last quarter saw substantial insider selling of Snap shares. In total, insiders sold US$23m worth of shares in that time, and we didn't record any purchases whatsoever. In light of this, it's hard to argue that all the insiders think that the shares are a bargain.

Insider Ownership of Snap

Many investors like to check how much of a company is owned by insiders. High insider ownership often makes company leadership more mindful of shareholder interests. Snap insiders own 24% of the company, currently worth about US$21b based on the recent share price. I like to see this level of insider ownership because it increases the chances that management is thinking about the best interests of shareholders.

Insiders Aren't Showing Optimism (Yet)

Insiders sold Snap shares recently, which is not surprising given that the stock at one point tripled up during the last 12 months, yet they didn't buy any. As the company faces the headwinds, observing the high insiders share of over 23% will give some indications about the outlook from the management.

It is good to see high insider ownership, but insider selling leaves us cautious. So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company.

To assist with this, we've discovered 3 warning signs that you should run your eye over to get a better picture of Snap.

If you would prefer to check out another company with potentially superior financials, then do not miss this free list of interesting companies with high returns on equity and low debt.

For this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions, but not derivative transactions.

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com