Yahoo Finance

Yahoo Finance How to Use Comparable Company Analysis to Derive the Value of Any Stock

Kay Ng recently wrote a piece on uncovering the value of a stock through its historical trading levels. While Kay?s article serves as a great introduction to valuation, I would like to take it one step further and compare a stock with its peer group in a technique known as ?comparable company analysis?/ ?trading comparables,? or simply ?comps? for short.

Why comps?

When it comes to valuation, a comps model provides the most bang for your buck from an opportunity cost standpoint. Armed only with a basic level of Excel, an investor can draw up a rough comps table within an hour ? a significantly shorter time frame than, say, a discounted cash flows approach, which would require days, if not weeks, of work to fine tune. In fact, due to this simplicity, professional money managers and analysts rely on the comps model or other comparative analysis over any other method in determining the intrinsic value of a security.

Callidus Capital Corp. (TSX:CBL) comps. Note the specialty finance and alternative mortgage lender peers, along with industry standard multiples (Source: company investor presentation)

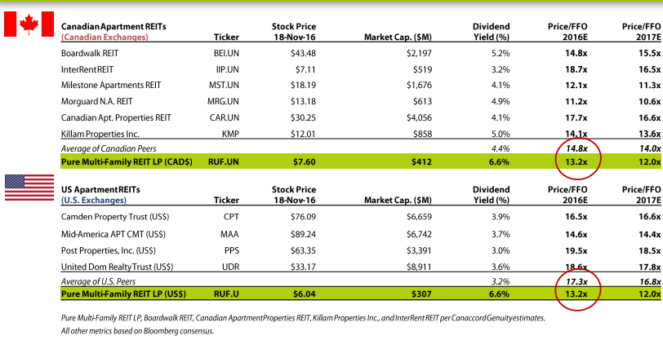

Pure Multi-Family REIT comps. Note the geographic groupings of the comparable companies and industry standard multiple (P/FFO). (Source: company investor presentation)

The basics

The first step to running a comps table is to select a group of similar companies with similar market caps, life cycles, and geographic and revenue segments. This is arguably the most important step of the model, as differing companies will defeat the purpose of a ?comparable? approach, and you will not be able to derive an implied price for the shares (more on this later).

The second step in building the comps model is to select the appropriate metrics to compare your firm against its peers. While the P/E ratio is nice, remember that it?s not the one-size-fits-all ratio that should be used for every company under the sun, especially for those with little or no earnings; for example, a young growth stock with no earnings stream, such as Canopy Growth Corp (TSX:CGC), would typically be valued with the enterprise-value-to-sales multiple. Therefore, learning the industry-standard multiples will greatly enhance your valuation skills.

The third step ? expanding on the second step ? is to include some metrics about the company that are unique to its industry, such as the reserve ratio for oil companies, net asset value (NAV) for miners, net operating income (NOI) for REITs, same-store sales for retailers, etc. These additional metrics, when viewed alongside the industry-standard multiples, will provide key insights into why a stock is trading where it is.

One way to get an idea of what to use is to start by looking at analyst reports, company filings (especially the management discussion and analysis), or the company?s investor presentations to get a sense of what multiple/metric to apply.

Finally, the last step is to determine why a company is trading the way it is. For example, if your target company is trading significantly below its peers, then it?s up to you to determine why it?s trading at such a level and whether or not it is justifiable given the company?s operating performance. Likewise, if the company is trading above its peers, then you must carefully determine why the market is paying a ?premium? for this company.

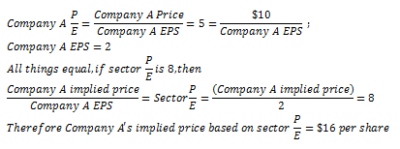

Moreover, you can also take this one step further and determine an ?implied? price by the average valuation of the company?s peers and whether or not the stock will eventually trade close to the market?s valuation. For example, if Company A is trading at five times its earnings with a current price of $10 per share, and the sector average is eight times earnings, all things equal, Company A should be trading closer to $16 per share.

Example of implied price calculation using the P/E ratio (Source: author generated)

Conclusion and caveats

Valuation is generally a very subjective endeavour, and not even the comps model is without its flaws. For example, the analysis requires significant judgment (will discount/premium gaps close?) as well as a reliance on market rationality (similar companies trading similarly). That being said, the comparable company analysis is still one of the most powerful tools in all of valuation, and, with practice, it might become your go-to technique to separate the winners from the losers.

The Exclusive Buy "Signal" You Can't Ignore

Over the course of The Motley Fool U.S.'s 23 year history, this rare buy "signal" has generated massive wealth for those that have been smart enough to pay attention to it. It's so rare, that it's happened less than two dozen times... but when it does - it's made investors undoubtedly rich. If you're interested in knowing the stock behind this rare buy "signal" - and you're excited to take advantage of this golden opportunity, then you're going to want to read this. Click here to unlock all the details behind this new recommendation from Stock Advisor Canada.

More reading

Fool contributor Alexander John Tun has no position in any stocks mentioned.

The Exclusive Buy "Signal" You Can't Ignore

Over the course of The Motley Fool U.S.'s 23 year history, this rare buy "signal" has generated massive wealth for those that have been smart enough to pay attention to it. It's so rare, that it's happened less than two dozen times... but when it does - it's made investors undoubtedly rich. If you're interested in knowing the stock behind this rare buy "signal" - and you're excited to take advantage of this golden opportunity, then you're going to want to read this. Click here to unlock all the details behind this new recommendation from Stock Advisor Canada.

Fool contributor Alexander John Tun has no position in any stocks mentioned.