Yahoo Finance

Yahoo Finance If China Tech Thought 2018 Was Bad, Wait Till This Year Unfolds

(Bloomberg) -- Sign up for China Rising, a new weekly dispatch on where China stands now and where it's going next.

Many of China’s proudest technology champions were only too glad to put 2018 behind them. This year may present even bigger challenges.

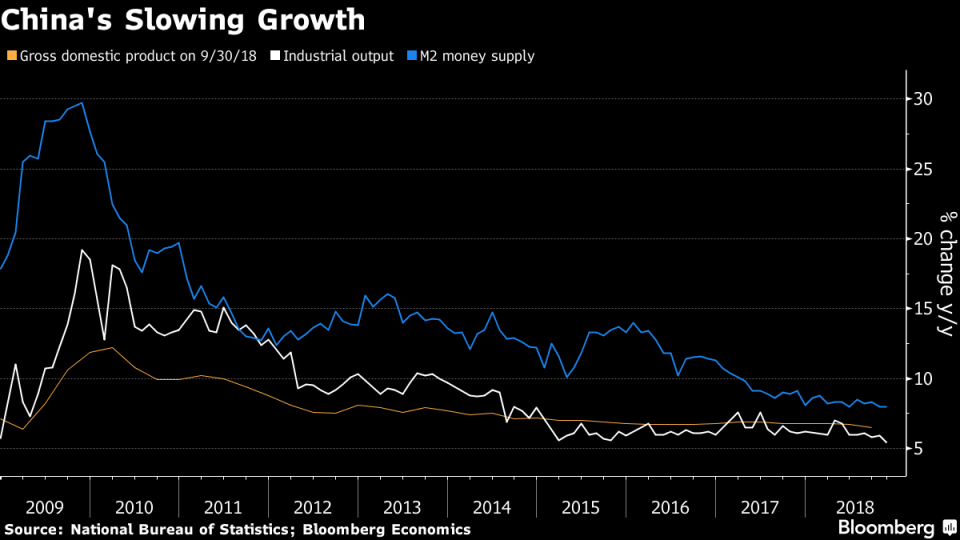

From brushes with the law and a jaw-dropping market rout to regulatory clampdowns and even destructive American action, the country’s largest corporations weathered a litany of seemingly random catastrophes. In 2019, they face a common, far more inexorable enemy: a rapidly cooling home economy.

China’s deceleration will create ripple effects across the corporate landscape. Businesses already contending with tighter credit face an even tougher environment as tensions with the U.S. dampen industrial activity and consumer sentiment in the world’s second largest economy. Apple Inc.’s shock outlook-cut only exacerbates fears that it’s losing steam more rapidly than anticipated.

“Sentiment isn’t great. There’s still macro uncertainty, regulatory headwinds, competition in China internet where everyone needs to invest more to counter slower user growth,” said Jerry Liu, an analyst with UBS. “Companies in China on average traded higher than the U.S. but now valuations have come down and converged. It shows you the headwinds China internet is facing.”

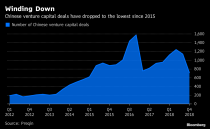

All that translates into real consequences for China Tech Inc. Mega-fundraisings -- the lifeblood of a young internet sector -- may dissipate: venture capital deal-making is at its lowest since 2015 even as funding sizes shrink. Consider Ofo, the high-profile pioneer of China’s bike-sharing boom that almost presented the country’s biggest startup failure in years.

As for deeper-pocketed juggernauts from Alibaba Group Holding Ltd. to Tencent Holdings Ltd., they can no longer lean as heavily on their home market to keep the top line humming. Morgan Stanley estimates revenue among the Chinese internet stocks it covers will grow 29 percent on average in 2019 -- dipping below 30 percent for the first time since at least 2015.

That’s a sea change from the start of 2018, when it seemed as if Tencent and its ilk were on the brink of fulfilling a dream of upstaging Silicon Valley.

Things started going off the rails in the second half of last year as Huawei Technologies Co. finance chief Meng Wanzhou and JD.com Inc.’s billionaire-founder Richard Liu found themselves in legal hot water (for different reasons). Didi Chuxing went from hometown darling for the way it beat Uber to public enemy No. 1 when two of its drivers allegedly killed women passengers. Xiaomi Corp. and Meituan Dianping, two of China’s most promising emergent tech concerns, have lost billions in market value since their debut.

Tencent, the poster child for China’s unprecedented economic boom, shed more than $200 billion of market value after regulators choked off its games pipeline, leading the biggest selloff in Asian technology shares in a decade. The MSCI Asia Pacific Information Technology Index dived 21.2 percent in 2018: the biggest annual drop since the 2008 recession.

“2018 marked the beginning of another transition for China internet companies, as a tougher-than-expected macro backdrop has led to softer sales,” Morgan Stanley analysts led by Grace Chen and Alex Poon wrote. “Macro risk is rising.”

In 2019, China’s tech glitterati need to confront a number of issues. Economists see growth slowing to an annual pace of 6.2 percent in 2019, the weakest pace since 1990.

The trade conflict is weighing on activity, hurting corporations like Alibaba and JD that depend directly on home consumption. A corresponding decline in advertising hurts Tencent and Baidu Inc. For private companies like Bytedance Ltd., the funding spigot they draw on to super-charge growth is starting to dry up.

Less quantifiably, China is in the throes of the most severe digital crackdown in its history, a censorship push that shows no signs of letting up. That will force virtually every internet player to invest time and money training bots and staff to root out content the ruling Communist Party deems taboo.

To many, the market rout is far from over, thanks to President Donald Trump’s campaign to contain China, starting with punitive tariffs. Depending on the state of the markets, the IPO pipeline may constrict in 2019 as mega-startups that haven’t listed, such as Didi or Alibaba-backed Ant Financial, put off their coming-out parties.

“You can blame Donald Trump,” said Mitchell Green, a Santa Barbara-based founding partner of Lead Edge Capital, which manages $1.5 billion of assets and backs Alibaba and Tencent Music.

Longer term, China’s tech aspirants must look beyond a saturated home to sustain double-digit growth. As Alibaba’s Jack Ma told a World Trade Organization forum in Geneva in October: “If you’re not globalized, you’re dead.” But once-frenetic deal-making in U.S. startups has all but evaporated and others, such as Huawei and JD, have become much quieter about their global ambitions.

However things shake out in 2019, China is hell bent on becoming a tech powerhouse in the next five years. Xi Jinping’s controversial blueprint to transform China from smokestacks to technology cradle -- his so-called Made in China 2025 plan -- is raising hackles among Washington and its allies. And thus-far reflexive attempts to contain the budding superpower can only intensify.

“We’re not in a trade war now, we’re in a geopolitical cold war started by the U.S.,” Alibaba Vice Chairman Joseph Tsai said at a conference in late 2018.

Perhaps no company better personifies the perceived threat than Huawei. Once a purveyor of pedestrian telecoms equipment, it’s overtaken Apple in smartphones and is amassing a lead in fifth-generation mobile while preparing to take on some of America’s biggest chipmakers.

But the country’s largest tech company by revenue has learned first-hand how vague suspicions can manifest in abrupt action. Even before Meng’s arrest, Trump’s administration had invoked its name in blocking a Qualcomm-Broadcom merger that would’ve been the largest deal ever, saying it would hand the lead in 5G to China. Now, it’s been blocked from selling its gear from Australia to New Zealand, facing opposition even in Papua New Guinea. Just days ago, an executive of the company was arrested in Poland on allegations of spying for the Chinese government.

To be sure, not everyone is so relentlessly downbeat. At the end of the day, investors such as Xia Mingchen believe staying the course will pay off. “We don’t believe the U.S.-China trade war will have a very significant impact on the capital flow into China from outside of the country,” said the managing director of Hamilton Lane, which has $452 billion of assets under management. “The market is huge, with a big population, and is fast-growing compared to Western countries.”

--With assistance from Jeffrey Black.

To contact the reporters on this story: Edwin Chan in Hong Kong at echan273@bloomberg.net;Lulu Yilun Chen in Hong Kong at ychen447@bloomberg.net;David Ramli in Beijing at dramli1@bloomberg.net

To contact the editors responsible for this story: Robert Fenner at rfenner@bloomberg.net, Reed Stevenson

For more articles like this, please visit us at bloomberg.com

©2019 Bloomberg L.P.