Yahoo Finance

Yahoo Finance China's New Nasdaq Is for Traders Who Want to Experiment

(Bloomberg) -- China’s newest stock-trading venue is more than just an effort to keep start-ups at home. It’s a laboratory for rules that could eventually ripple across the nation’s $7.6 trillion equity market.

Regulators waived restrictions on how companies are priced when they list and eased reviews for applicants seeking to go public on the so-called technology board, while introducing curbs on retail investors that dominate China’s broader markets. Nearly 100 firms, from state-owned China Railway Signal & Communication Corp. to cloud storage provider UCloud Technology Co., have applied to list through instruments including what could be the first ever China depositary receipt.

The tech board’s rules, based on concepts found in the U.S. and Hong Kong, are seen as a tacit acknowledgement that Chinese authorities’ hands-on approach to governing stocks has limits. While wider adoption of the regulations would align Chinese bourses closer with their global peers, the magnitude of swings once the venue starts operating could be a key determinant in how fast the regulations are replicated.

“The Sci-Tech board is the breeding ground for major listing reforms,” said Alexious Lee, head of China capital access at CLSA Ltd. “We will see the Chinese market’s mechanisms get closer to global standards.”

Stocks may start trading on the new venue as early as June as officials say they will limit the review period for IPO applications to three months. Li Chao, vice chairman of the China Securities Regulatory Commission, said on March 29 that there may be disagreements over the qualification of potential IPOs in the initial phase when the registration system is being tested, and early trading may be volatile.

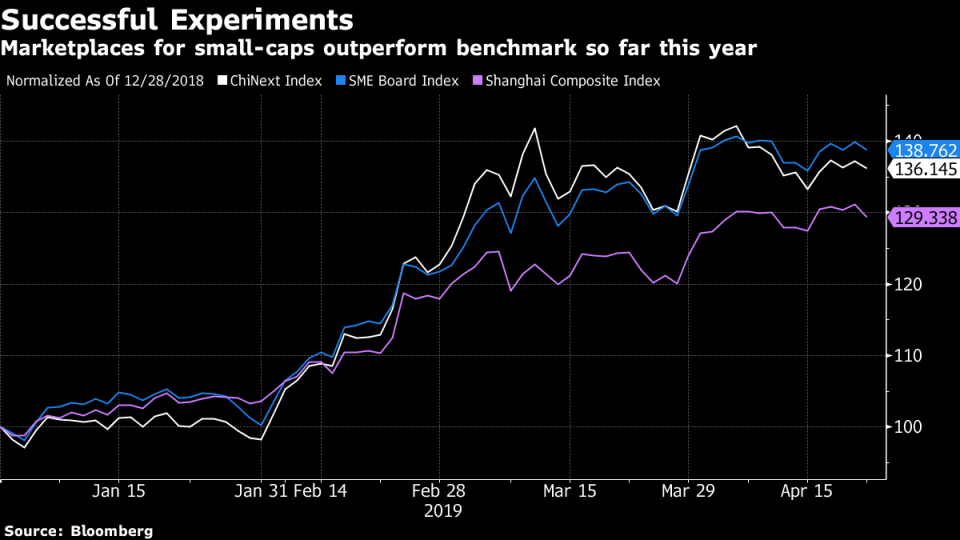

Some previous attempts at creating new trading venues, such as the strategic emerging industries board, haven’t yet seen fruition. The ones that reached completion, such as the ChiNext in Shenzhen, imposes a narrower band within which a stock can swing. They also include rigid regulatory vetting and keep out pre-profit companies.

Shanghai’s Nasdaq-style marketplace will have no such restrictions. The stock exchange this year clarified that companies will be free to “price according to the market,” in contrast to informal guidance that has kept Chinese IPO valuations at or below 23 times earnings.

Regulators also allowed for shares with unequal voting rights, a controversial step that grants founders greater control, and will only permit investors with half a million yuan worth of assets in their trading account and two years of experience, which is outside the reach of most retail clients.

China Asset Management and ICBC Credit Suisse Asset Management Co. are among firms who have been permitted to create a first batch of seven mutual fund-type products, where underlying assets are shares on the tech board, the official China Securities Journal reported on Tuesday. China Galaxy Securities Co. predicts that more than 200 funds will be set up to allow access for retail investors, according to the report.

The preference for institutional investors will probably ensure that early trading isn’t as volatile as when the ChiNext started operating, though there will be some speculation, according to Gang Zhang, a Shanghai-based strategist at Central China Securities Co.

Luo Huizhou, an analyst at Pacific Securities Co., eventually sees the tech board competing with the ChiNext. The CSRC didn’t reply to a fax seeking comment on whether the tech board’s rules will be replicated across Chinese exchanges.

“It is better able to test reforms given its lack of historical burdens,” Zhang said. “The tech board is the biggest move in China’s capital market in the last 20 years.”

(Updates with information on tech board-linked products in ninth paragraph.)

To contact Bloomberg News staff for this story: Lucille Liu in Beijing at xliu621@bloomberg.net;Ken Wang in Beijing at ywang1690@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues, Sharon Chen

For more articles like this, please visit us at bloomberg.com

©2019 Bloomberg L.P.