Yahoo Finance

Yahoo Finance Challenge for Trump: Job growth is slowing

The economy powered forward in 2017, but there’s at least one warning sign for 2018: the pace of job growth has slowed down considerably.

Employers created 148,000 jobs in December, a subpar showing, given that economists expected about 190,000 new jobs. But overall, the economy created more than 2 million jobs in 2017. That’s healthy.

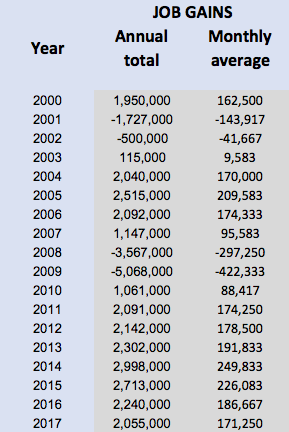

But not quite as healthy as it used to be. Job gains averaged 171,000 per month in 2017, down from 187,000 the year before. The pace of job growth has actually been slowing for three years, after peaking in 2014 at 250,000 per month. Here are the numbers:

Democrats and Republicans tend to see political implications in these types of economic numbers, blaming or crediting their favored politicians for the outcome. But the pattern of job creation probably has little or nothing to do with the policies of President Trump, or President Obama before him. In other words: Job growth isn’t slowing because of something Trump is doing.

Instead, the trendline actually represents a fairly predictable cycle as the economy began to recover from the deep recession that ended in 2009. Job growth peaked in 2014 not because of any specific Obama policy, but because employers simply needed to hire people to keep up with demand, after shrinking dramatically during the recession. And job growth is now slowing as most people who want a job have found one, with employers starting to face labor shortages.

The most important implication for 2018 is probably this: We’re in the late stages of an economic expansion, and job creation could continue to slow. That’s not necessarily bad. “The biggest problem of the American labor market is becoming too few workers rather than too few jobs,” economist Russell Price of Ameriprise wrote to clients recently. “We expect the pace of job growth to slow in 2018 simply due to the fact that there are fewer people available to be brought back into the job market.”

With the job market tightening, economists expect wages to rise. But they’ve been expecting that to happen for a while, and they’ve been wrong. Wages grew just 2.5% in 2017, and with inflation at 2.2%, that means workers, on average, are barely getting ahead. Wage growth of 3% to 4% would be more assuring. If there’s an upside, it’s that tepid wage growth lets the Federal Reserve keep interest rates lower for longer, which is generally good for businesses.

Job growth matters because it helps determine how quickly the overall economy grows. GDP growth should be around 2.5% this year, which isn’t terrible, but it’s obviously below the 3% to 4% growth rate Trump—and many economists—would like to see. Moody’s Analytics predicts GDP growth will hit 2.8% in 2018, partly because the tax cuts Trump just signed into law will provide a bit of fiscal stimulus. But it will fade quickly. Moody’s Analytics predicts just 2.2% growth in 2019. And the firm’s chief economist, Mark Zandi, recently told Yahoo Finance the next recession could hit around 2020.

One way to boost growth would be to expand the labor force, since more people working means more people spending money. It’s possible some economic dropouts who gave up looking for work could rejoin the labor force, although their prolonged absence has been another puzzle economists have been unable to solve. More immigration would help too, but that’s not something Trump supports. So the stage seems set for sustained moderate growth, but not much more.

Confidential tip line: rickjnewman@yahoo.com. Encrypted communication available.

Read more:

Rick Newman is the author of four books, including Rebounders: How Winners Pivot from Setback to Success. Follow him on Twitter: @rickjnewman