Yahoo Finance

Yahoo Finance Canadian Value Investors: 2 Ridiculously Cheap Stocks

Written by Kay Ng at The Motley Fool Canada

In today’s high inflation, rising interest rate environment, it’s insufficient for a stock to just be cheap. Canadian value investors would be better served to look for stocks that are both cheap and pay them well. Here are some ridiculously cheap dividend stocks you can explore.

Look for value in the energy sector

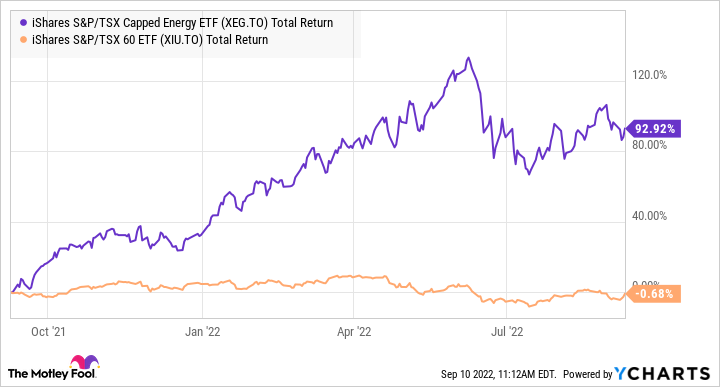

The energy sector has outperformed the market in the last one, three, and five years due to higher energy prices. The one-year total return shows a biased view in a favourable operating environment for the energy sector.

XEG and XIU Total Return Level data by YCharts

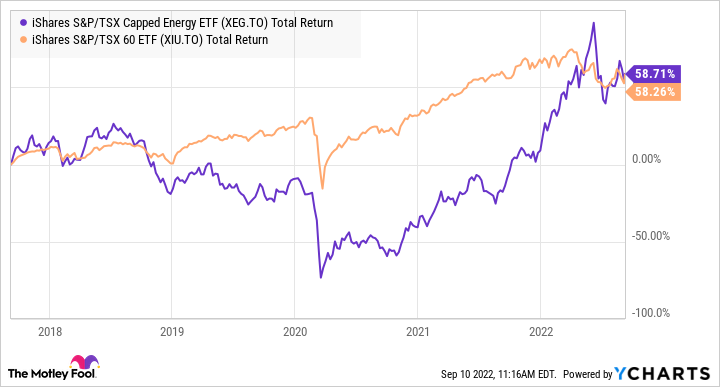

The three-year total return is more telling, as it illustrates the volatility that investors must bear when investing in the energy sector.

XEG and XIU Total Return Level data by >YCharts

And it was a close win for the energy sector over the last five years.

XEG and XIU Total Return Level data by YCharts

Stan Wong, portfolio manager at Scotia Wealth Management, stated on BNN last week that “Energy has a major supply/demand imbalance, along with major under-investment over the years. So, pricing can remain pretty firm with demand steady.”

A cheap energy stock paying a good dividend

XEG Total Return Level data by YCharts

Parex Resources (TSX:PXT) has underperformed the energy sector in the last one and three years, but it has outperformed in the last five and 10. This is because the oil stock generally remains under-leveraged versus its peers. In fact, its net debt is zero. And it tends to buy back shares. Because of relatively high oil prices with Parex particularly enjoying premium Brent oil prices, its profits have spiked. It now trades at about 4.1 times trailing earnings and 2.7 times forward earnings.

Moreover, it started paying a quarterly dividend in September, which should improve the stability of its returns and possibly boost total returns for investors. Its trailing 12-month (TTM) payout ratio was approximately 20% of free cash flow. Specifically, it had about $341 million free cash flow left over after capital investments and dividend payments!

Parex doubled its dividend year over year. Its dividend yield is just over 4.7% at $20.97 per share at writing.

One more energy-related dividend stock that’s ridiculously cheap

Another energy-related dividend stock that is mispriced is Canadian Western Bank (TSX:CWB). It trades at a lower multiple than its bigger bank peers. First, it is a smaller bank. Second, it has about 31% of its loans in Alberta. The province’s economy can be more unpredictable because of volatile energy prices.

The Canadian bank’s business has already significantly diversified away from Alberta over time. British Columbia and Ontario are where 33% and 24%, respectively, of its loan portfolio is. In the last reported quarter, it saw loan growth in all three provinces with its consolidated loan portfolio seeing growth of 9% year over year. Its gross impaired loans as a percentage of gross loans were fairly low at 0.53% fiscal year to date, down 33 basis points year over year.

The bank remains profitable through economic cycles and has maintained a respectable dividend-growth streak of 30 consecutive years through three recessions! At $24.79 per share, the bank stock trades at about 6.8 times earnings. Given the right environment, it can appreciate to its long-term normal valuation, which represents about 66% upside. Meanwhile, investors get paid well to wait. CWB stock offers a juicy yield of 5%. Its TTM payout ratio is sustainable at 39%.

The post Canadian Value Investors: 2 Ridiculously Cheap Stocks appeared first on The Motley Fool Canada.

Should You Invest $1,000 In Canadian Western Bank?

Before you consider Canadian Western Bank, you'll want to hear this.

Our market-beating analyst team just revealed what they believe are the 5 best stocks for investors to buy in August 2022 ... and Canadian Western Bank wasn't on the list.

The online investing service they've run for nearly a decade, Motley Fool Stock Advisor Canada, is beating the TSX by 27 percentage points. And right now, they think there are 5 stocks that are better buys.

See the 5 Stocks * Returns as of 8/8/22

More reading

Fool contributor Kay Ng has positions in Canadian Western Bank and Parex Resources. The Motley Fool has no position in any of the stocks mentioned.

2022