Yahoo Finance

Yahoo Finance Better Buy: Berkshire Hathaway vs. American Express

Berkshire Hathaway Inc. (NYSE: BRK-A)(NYSE: BRK-B) has made for one of the great investments of all time. Under legendary investor and CEO Warren Buffett, maybe no other company has created as many billionaires as Berkshire. One of Buffett's best investments has been American Express Company (NYSE: AXP), which has been a staple holding in Berkshire's portfolio for decades. Berkshire owns 17.5% of the company, worth about $15.4 billion. That's a nearly 12-fold increase in value from the $1.29 billion Berkshire paid.

And it gets even better: Berkshire collects over $212 million in dividends from American Express each year, an incredible 16.5% yield on Berkshire's cost basis for its American Express investment.

Still, which is the better investment now? On one hand, there's the highly diversified cash cow that is Berkshire, while on the other, you have AmEx's highly profitable -- but also more leveraged -- business with incredible growth prospects.

Frankly, there's a good case to be made for both companies today, but it really depends on what you -- the person who'll own the stock -- are looking for. If you're more interested in a company that's built to ride out any economic condition and limit your downside risks, Berkshire wins. But if you're willing to take on more exposure to consumer spending and economic cycles in exchange for better growth prospects, American Express comes out ahead.

Image source: Getty Images.

And that should put American Express in the "win" column for the majority of investors. Keep reading to learn why.

Comparing two very different companies

One of the biggest challenges to comparing Berkshire and American Express is that they operate in entirely different industries. Berkshire is one of the most diversified businesses on the planet, with holdings across financial services, utilities, industrial goods, and consumer products. The vast scale and scope of its offerings make it a lower-risk holding, since its core insurance, utility, and dividends paid by its equity holdings are both substantial and largely recession-resistant.

American Express, on the other hand, makes a living by extending credit to individuals and businesses, and a substantial amount of that debt -- charges on American Express cards -- is unsecured. This along with a more leveraged balance sheet (it routinely carries more debt than cash) make American Express a higher-risk investment than Berkshire Hathaway, particularly during weaker economic periods.

Here's an example of how that can play out:

This is a "worst-case" scenario, showing how much farther American Express shares fell from the 2007 peak to the 2009 bottom during the global Financial Crisis. Needless to say, many investors were fearing the worst for every financial institution, including Amex, which received $3.4 billion in TARP funds from the U.S. federal government in January of 2009.

However, this risk has proved to be more perception than reality. For instance, even during the Financial Crisis -- the worst economic downturn in almost nine decades now -- American Express was probably further from real trouble than it seemed, and it was able to fully repay the government before the end of 2009. Yes, its profits did fall sharply from over $4 billion in 2007 to $2.1 billion in 2009, but it remained cash-flow positive and was probably less at risk than it may have seemed.

And anyone who recognized the opportunity and bought AmEx near the market bottom has enjoyed 10-fold total returns, even as Berkshire tripled in value:

AXP Total Return Price data by YCharts.

But it's one thing to think you can ride out a downturn this sharp, and another thing entirely to do it. And that's something investors must consider deeply.

Which is the better deal right now?

From a valuation perspective, both AmEx and Berkshire are reasonable. Berkshire trades for less than 1.4 times its book value, a measure Warren Buffett uses to value the company. And while that's not the dirt-cheap 1.2 times it has fallen to in the past, it's cheaper than it has been for most of the past few years:

BRK.B Price to Book Value data by YCharts.

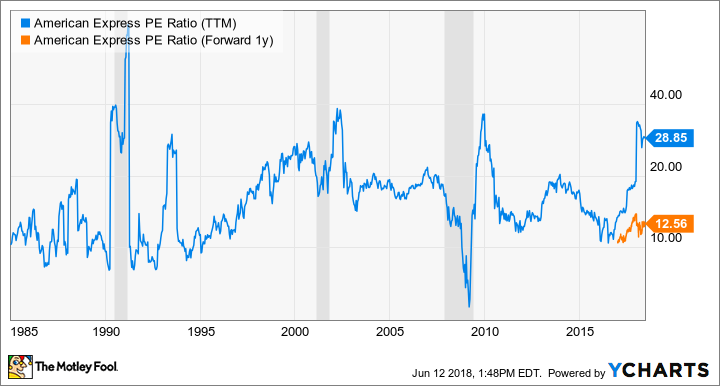

American Express is also reasonably priced based on its expected 2018 earnings, trading for about 12.6 times estimates. That's actually on the high end for its forward earnings multiple over the past year, but when compared to the P/E multiple investors have proven willing to pay for the company in the past, it's a very good deal:

AXP PE Ratio (TTM) data by YCharts.

Paying less than 13 times AmEx's 2018 earnings should work out very well for long-term investors.

Verdict: AmEx for one simple reason

Investors looking for more "defensive" stocks to fortify their portfolios might prefer Berkshire, and I wouldn't argue against that. The company isn't bulletproof, but it offers some decent recession-resistance that makes it an appealing "safer" stock to buy. But when it comes to generating the most wealth over the long term, I think Berkshire will come up short versus American Express.

AmEx will almost certainly be a more volatile stock to own during market downturns, but the company is primed for years of growth. Factor in an aggressive share buyback program that's reduced the share count by 21% in the past five years alone and a solid history of dividend growth, and American Express is not only likely to outperform Berkshire in the years ahead, but beat the market, too.

More From The Motley Fool

Jason Hall owns shares of American Express. The Motley Fool owns shares of and recommends Berkshire Hathaway (B shares). The Motley Fool has a disclosure policy.