Yahoo Finance

Yahoo Finance Adient Stock: Still Undervalued After Johnson Controls Spinoff

- By Ben Reynolds

(Updated Jan. 16 by The Financial Canadian)

Occasionally, investors are faced with the unique scenario in which one of their holdings spins off selected assets as new securities.

One of the most notable cases in recent history was in 2013 when AbbVie (ABBV) was spun-off from its parent company, Abbott Laboratories (ABT). Both of these companies are strong dividend growth stocks based on The 8 Rules of Dividend Investing.

Warning! GuruFocus has detected 4 Warning Sign with ABBV. Click here to check it out.

The intrinsic value of ABBV

Recently, another one of these spinoffs occurred. Johnson Controls (JCI) spun off its automotive interiors business under the name Adient (ADNT).

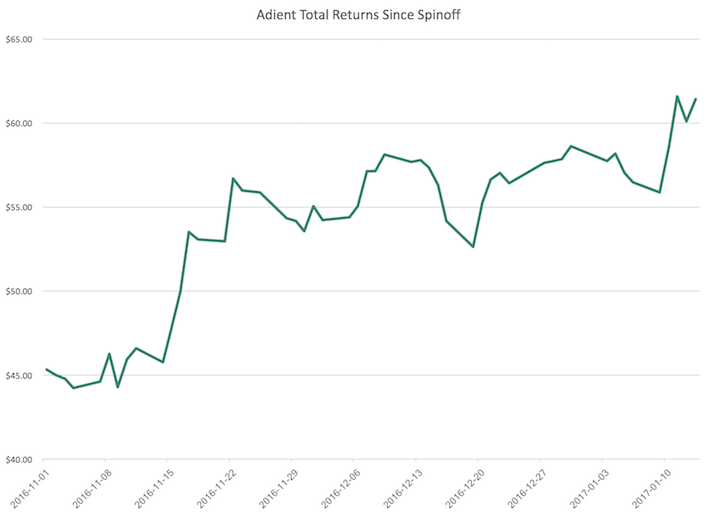

Since the spinoff, Adient's stock has rewarded shareholders handsomely. The stock has increased ~36%.

Source: Yahoo! Finance

This post will discuss the future investment prospects of Adient in detail. Namely, this article is aiming to help investors discern whether they should continue to hold on to Adient shares that were received due to ownership of Johnson Controls.

Business overview

Adient's origins can be traced back to 1985 when Johnson Controls acquired Hoover Universal and officially entered the automotive seating business. Over time, Johnson Controls expanded its portfolio of automotive seating products with the following bolt-on acquisitions:

Naue Group.

Lahnwerke.

Prince Corp.

Becker Group.

Lander Automotive.

Benoac Fertigtelle GmbH.

Michel Thierry Group.

Hammerstein Group.

Adient's inception as a publicly traded company is much more recent than most of the companies covered on Sure Dividend. The company first traded hands on the New York Stock Exchange on Oct. 31, 2016. I'll begin this business analysis by describing the details of the stock's spinoff.

Johnson Controls' shareholders received one share of Adient for every 10 shares of Johnson Controls . The spinoff was completed on Oct. 31, 2016, and the record date for the transaction was Oct. 19. Fractional shares of Adient (which would be received in the event that Johnson Controls' shareholders did not hold shares in multiples of 10) were not distributed - instead, shareholders received cash.

Adient is currently the largest automotive seat supplier in the world. Its size and scale is impressive:

230-plus locations globally.

25 million-plus seat systems per year.

75,000 employees.

Adient's operations are diversified into two reporting segments, which share roughly the same proportion of sales. These operating segments are seating and interiors.

The company also reports earnings in four geographic operating segments:

Americas (34% of sales).

China (30% of sales).

Europe/Africa (29% of sales).

Asia/Pacific (7% of sales).

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 5

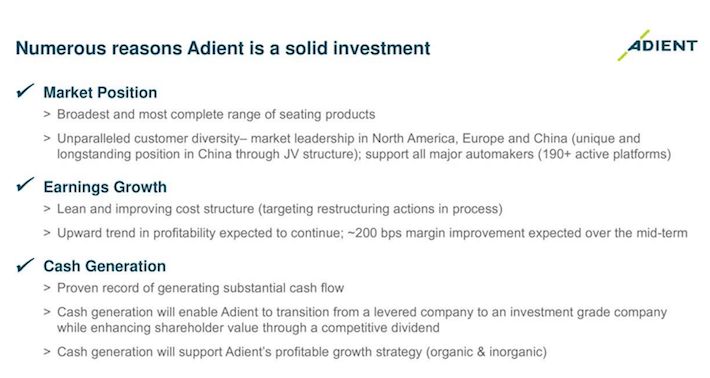

From an investor's point of view, there are a few things that stand out about Adient.

The first is its market leadership. Adient has one of the broadest ranges of seating products on the market. This has led to the incredible diversification among its customer base. The company supports all major automakers with more than 190 active platforms.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 4

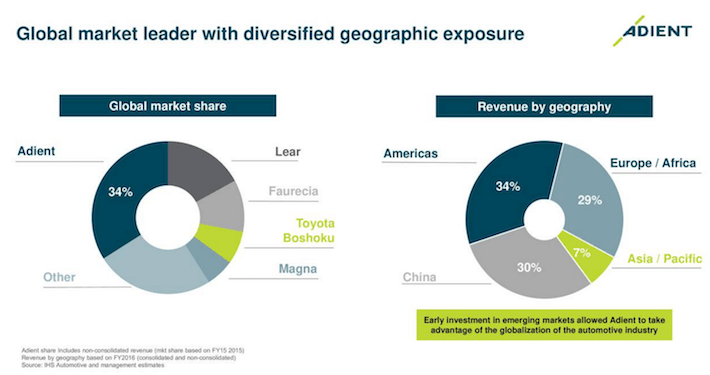

Adient's customer diversification has also led to substantial geographic diversification in terms of the company's revenues. Although the company has some very American aspects, with operational headquarters in Detroit and a stock that trades on the New York Stock Exchange, it is tax domiciled in Ireland and only 34% of its revenues are generated in the Americas.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 8

Because of this diversification, Adient has leadership of the global automotive seating products industry at 34% market share.

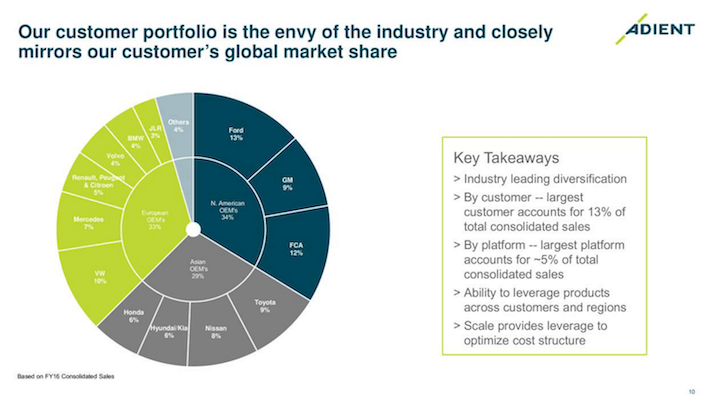

Adient's customer portfolio is comprehensive. Their customer breakdown by geography mirrors their customer's global market share. Notable domestic industry names that are Adient's customers include Ford (NYSE:F) and General Motors (GM) along with a variety of international names.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 10

To serve this international customer base, Adient's operational locations are globally diversified. In its interiors segment alone, it has a physical presence in 17 different countries across each of its four reporting segments.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 13

Now that the size and scale of Adient is understood, I will move on to identify the company's growth prospects.

Growth prospects

One of the largest drivers of growth for Adient will be the expansion of the overall automotive seating market. Similar to Coca-Cola (KO), Adient operates in a growing industry, which will lead to revenue growth even if the company's market share remains constant.

There are a few different reasons why Adient's industry is expanding. Each will be identified and explained here.

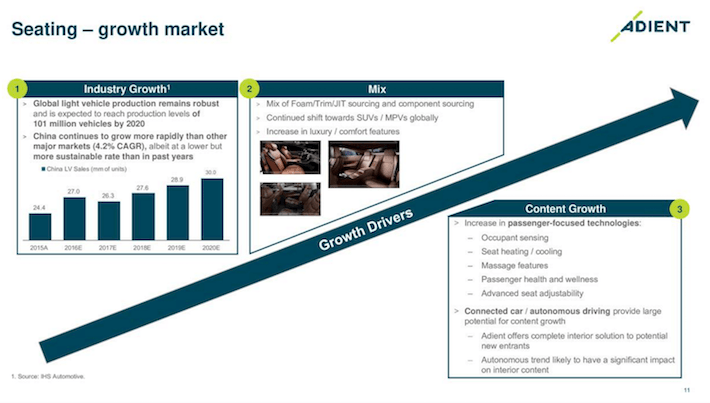

The first is the continued growth in global automotive production. More cars means more seats, which is beneficial for Adient. Global light vehicle production (the main group of vehicles that Adient produces seats for) is expected to reach production levels of 101 million vehicles by 2020. There were 91.5 million automobiles produced in 2015; this estimate implies that production will grow at a ~2.0% CAGR through 2020.

Adient is poised to further benefit from the mix of automobiles produced. There is a continued demand shift toward SUVs as well as an increase in demand for luxury and comfort features in new automobiles. Both of these trends will boost Adient's revenues - premium features demand premium prices, after all.

Lastly, Adient's technology-related products are poised to surge during the coming years. Features like seat heating/cooling, in-seat massages and electronic adjustability are becoming more accepted and popular with the mainstream automotive consumer.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 11

Adient's growth prospects also benefit from its entrance into new markets and relationships with new customers. The company is exploring entry into commercial vehicle seating, railway seating and aircraft seating. If these new endeavors prove successful (which is likely given the company's automotive expertise), then this will be a boost to Adient's future revenues.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 16

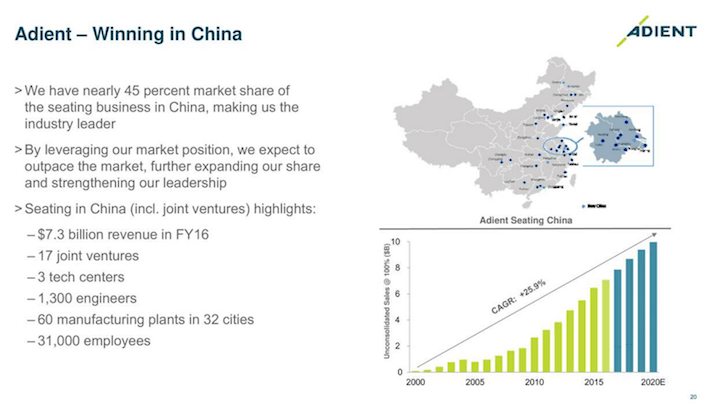

The company's presence in China presents yet another growth opportunity. Growth in this geographical market has been nothing short of incredible - Adient expects China's sales to grow at a ~26% CAGR through 2020.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 20

All things considered, the future looks bright for Adient.

Competitive advantage and recession performance

Adient operates in a low-margin business, and there is no doubt that it is the global leader in automotive seating production. The company's size and scale provides a distinct competitive advantage.

That being said, the automotive industry has not historically performed well during times of economic recession. The bankruptcy of General Motors during the 2008-2009 financial crisis is but a single example of this.

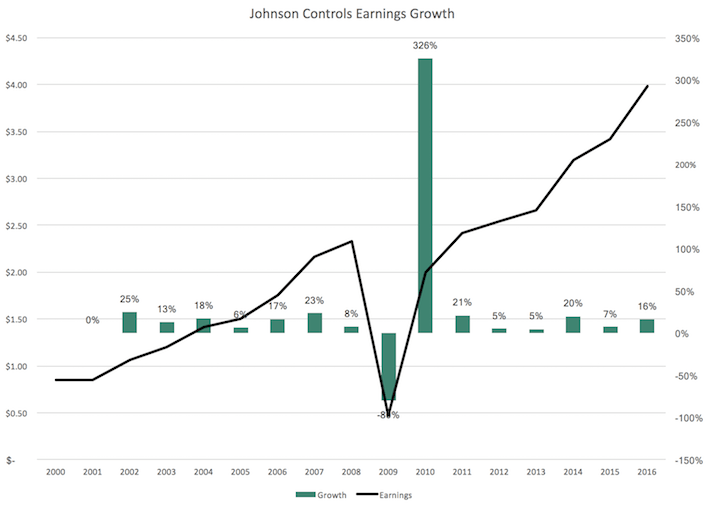

One way to assess the recession resiliency of Adient is to consider the effect of the global financial crisis on the earnings on Johnson Controls. Its EPS during this time period is as follows:

2007: $2.33.

2008: 47 cents (79.8% decrease).

2009: $2.00 (325.5% increase).

2010: $2.42 (21.0% increase).

2011: $2.54 (5.0% increase).

Although the company managed to barely remain profitable, Johnson Control's earnings were severely impacted by the global financial crisis.

Adient will have one major insulator if a recession was to materialize during the near term. The company has no debt maturing before 2021. This will allow the company an adjustment period post-spinoff before any debt needs to be refinanced or repaid.

Source: Adient Investor Presentation, Deutsche Bank Global Auto Industry Conference, slide 37

Adient (or, rather, the former parent company Johnson Controls) has not historically performed well during times of economic recession, which is in line with the rest of the automotive industry. However, the company has no near-term debt maturities, which should allow it a period of adjustment before any debt is required to be refinanced. This will be particularly useful in the event of an economic recession in the near term.

Valuation and expected returns

It is difficult to estimate future returns for Adient shareholders.

Since the business was only recently spun off from Johnson Controls, we do not have a history to judge the competency of management or the profitability of the business.

However, we can make reasonable assumptions based on what is already known about the business. The first thing that I'll consider is the company's current valuation.

Despite being recently spun off, Adient has already filed its first 10-K. In that document, it reported GAAP earnings per share of ($16.36). The company was impacted by significant one-time legal and taxation charges due to its breakaway from Johnson Controls. For instance, Adient recorded $1.2 billion in selling, general and administrative expenses and $322 million of restructuring and impairment charges.

Looking at adjusted earnings will provide a more realistic assessment of the company's financial position. The following photo outlines the impact of significant items for Adient's fiscal 2016. Notice that 2016's number is significantly higher than in previous years.

Source: Adient 2016 10-K, page 26

In 2016, the impact of significant items was ~$2.6 billion. If we back this number out from the company's GAAP net income of $1.533 billion and replace it with the previous year's $409 million figure, we arrive at net income of $694 million for fiscal 2016. Dividing this net income by 93.7 million diluted shares outstanding gives adjusted diluted EPS of $7.41.

Based on this calculation and Adient's most recent close of $61.42, the company is trading at just 8.3 times 2016 earnings. On an absolute basis, this is very cheap.

For comparison, the Standard & Poor's 500 is currently trading at a price-earnings (P/E) ratio of ~26.1 and Johnson Controls has traded at a P/E ratio between 10.5 and 15.4 over the past 16 years (excluding one notable outlier that occurred during the global financial crisis).

Source: Value Line

Thus, based on the company's underlying earnings power, the company appears significantly undervalued.

We could also consider the company's valuation compared to its book value.

In its 2016 10-K, the company reported total shareholders' equity of $4.34 billion. Considering that the company has no preferred shares outstanding, we can divide this number by its 93.7 million shares outstanding to arrive at a book value per share of $46.32.

The company's most recent closing price was $61.42, which represents a price-book (P/B) ratio of 1.3. This compares favorably:

Old parent company Johnson Controls trades for 1.7 times book value.

Magna International (MG), a Canadian supplier of international automotive components, trades for 1.8 times book value.

Ford trades for 1.6 times book value.

General Motors trades for 1.3 times book value.

Thus, Adient appears to trade at a discount to other automotive companies (other than GM) based on the company's underlying assets.

In terms of earnings growth, looking at JCI's earnings growth prior to the spinoff can help in estimating future earnings growth for Adient.

Source: Value Line

Between 2000 and 2016, Johnson Controls compounded EPS from 85 cents to $3.98, which is good for a CAGR of 9.5%. An annual earnings growth rate of 7% to 9% seems appropriate for a high-quality industry leader like Adient.

That being said, Adient's earnings growth will likely not be smooth. I've already demonstrated how JCI's earnings were impacted significantly during the last recession. Adient's earnings will be similar in this regard.

The other component of expected returns is dividend payments. Adient has not yet paid a dividend to shareholders. This is because Adient is required to jump through legal hoops before it can legally pay dividends in the U.S., due to its headquarters being in Ireland.

Adient has not provided any guidance with regard to the payout ratio applied to its dividends. For the purpose of calculating expected returns, I'm going to assume that Adient will soon begin paying dividends with a yield of 2% (an approximation of the yield of the S&P 500 Index). While it's likely that the company's yield will actually be higher than this due to its low valuation, this is a conservative assumption.

Over the long run, expected shareholder returns for Adient will come from 2% dividend yield and 7% to 9% earnings growth for expected total returns of 9% to 11%. It is highly likely that these returns will be boosted by valuation expansion.

The end result is that investors in Adient will continue to see double-digit returns, even after the ~30% price run up.

Final thoughts

Adient offers investors a globalized investment opportunity at a very appealing valuation.

Although the company has not yet paid a dividend, even a 30% payout ratio would mean a dividend yield north of 3% because the company trades at less than 10 times earnings. Once the company begins to pay a dividend, it will rank favorably using The 8 Rules of Dividend Investing.

However, Adient may not be a suitable stock for risk-averse investors.

The automotive industry is not known for its recession resiliency. Adient's former parent company, Johnson Controls, saw earnings drop by 80% during a single year of the global financial crisis.

The company's eventual announcement of their dividend policy will provide more clarity on their investment thesis. At this point, the company remains undervalued - so Adient is still a hold for those who acquired the company through the Johnson Controls spinoff.

It is a buy for value investors looking to capitalize on an undervalued business that the market doesn't yet fully appreciate.

Disclosure: I am long Johnson Controls, Adient and Abbott.

Start a free seven-day trial of Premium Membership to GuruFocus.

This article first appeared on GuruFocus.

Warning! GuruFocus has detected 4 Warning Sign with ABBV. Click here to check it out.

The intrinsic value of ABBV