Yahoo Finance

Yahoo Finance Abercrombie (ANF) Q2 Loss Narrows, Stock Down on Tariff Woes

Abercrombie & Fitch Co. ANF incurred narrower-than-expected loss in second-quarter fiscal 2019. However, it reported earnings in the prior-year quarter. Moreover, the company’s top-line missed the Zacks Consensus Estimate and declined year over year. Further, management lowered sales view for fiscal 2019.

The company assumes the impact of List 3 and List 4 tariffs should hurt near-term results. These tariffs are likely to have an adverse impact of about $6 million on the company’s cost of goods sold and gross profit in the current fiscal year.

In fiscal 2019, the company expects gross margin to decline 50-90 basis points (bps) from 60.2% recorded in fiscal 2018. The downside can be attributed to combined unfavorable impact of currency and expected tariffs of about 60 bps. For the fiscal third quarter, gross margin is likely decline nearly 100 bps from 61.3% reported in the third quarter of fiscal 2018. Currency headwinds and anticipated tariffs to the tune of 90 bps primarily resulted in the downturn.

Abercrombie expects merchandise imports from China in the current fiscal year to be less than 20%, down from 25% last fiscal. Consequently, shares of the company slumped nearly 15% yesterday. In the past three months, the stock has lost 17.4% against the industry's 4.8% growth.

Nevertheless, this Zacks Rank #3 (Hold) company remains focused on achieving its long-term targets through the execution of the transformation efforts. In the United States, Abercrombie witnessed a robust start to back-to-school and expects the momentum to continue in the second half of fiscal 2019 backed by strength in products and solid marketing efforts.

In a separate press release, Abercrombie declared two major appointments to direct its Europe, Middle East, and Africa (EMEA) and Asia-Pacific (APAC) operations. Daniel Le Vesconte and Olga Wu are appointed as the Group Vice Presidents for the EMEA and APAC regions, respectively. These officials are likely to carry out the company’s strategies and boost brands to aid growth in the corresponding local markets.

Q2 Earnings & Sales

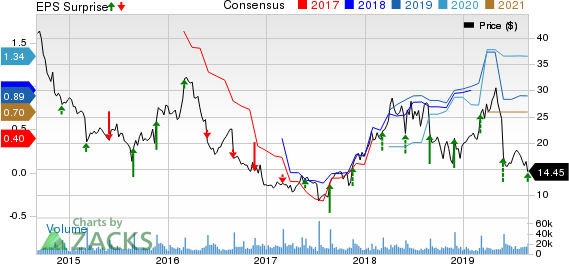

Abercrombie incurred loss of 48 cents per share in the second quarter, narrower than the Zacks Consensus Estimate of a loss of 52 cents. In the year-ago quarter, the company reported adjusted earnings of 6 cents. Bottom-line results were hurt by the negative impact of flagship store exit expenses to the tune of 50 cents.

Abercrombie & Fitch Company Price, Consensus and EPS Surprise

Abercrombie & Fitch Company price-consensus-eps-surprise-chart | Abercrombie & Fitch Company Quote

Net sales totaled $841.1 million, which missed the Zacks Consensus Estimate of $854 million and dipped 0.2% from the year-ago quarter’s sales of $842.4 million. On a constant-currency basis, the top line rose 1%.

Brand-wise, net sales improved 1% to $504.8 million at Hollister, while it dipped 2% to $336.3 million at the Abercrombie brand. From a geographical viewpoint, net sales grew 2% in the United States while dropped 4% in international markets.

Notably, digital business continued to perform well backed by robust momentum across both brands and geographies. Also, digital channel sales improved in the double-digit range during the quarter under review.

Comps in Detail

Comparable sales (comps) remained flat against 3% growth in the year-ago quarter. This was backed by favorable cross-channel traffic, compensated with lower conversion. Brand-wise, comps remained flat for both Hollister and Abercrombie brands.

Moreover, comps benefited from strong performance in the United States, wherein the metric improved 2%. This was partly offset by a 3% comps decline in international markets.

Margins

Gross margin contracted 90 basis points (bps) to 59.3% on account of higher average unit costs (AUC) due to product mix and a marginal fall in average unit retail (AUR). Further, the metric was hurt by increased promotions and markdowns, given the highly promotional U.S. retail environment.

Abercrombie incurred operating loss of $39.5 million compared to adjusted operating loss of $9 million in the prior-year quarter. Adjusted operating loss margin contracted 580 bps and fell 530 bps on a currency-neutral basis. Operating performance in the quarter was hurt by adjusted operating expenses to the tune of 470 bps owing to an unfavorable impact of 530 bps from the exit charges of flagship outlet.

Other Financials

Abercrombie ended the fiscal second quarter with cash and cash equivalents of $499.8 million and gross borrowings under its term-loan agreement of $253.3 million. As of Aug 3, 2019, inventories amounted to $487.1 million, reflecting 7% growth from the prior-year period. In the first six months of fiscal 2019, the company spent $94.2 million as capital expenditures.

Moreover, Abercrombie ended the fiscal second quarter with inventory up nearly 7% and expects the metric to grow low to mid single-digits at the end of the fiscal third quarter.

The company also bought back about 3.5 shares in second-quarter fiscal 2019. At the end of the fiscal second quarter, Abercrombie had nearly 5 million remaining under its current share repurchase authorization. So far in fiscal 2019, it returned $84.2 million via share repurchases and dividends.

On Aug 22, the company declared a quarterly dividend of 20 cents per share on the Class A shares. This is payable on Sep 16, 2019, to its shareholders of record as of Sep 6.

Store Update

Abercrombie has been closely working on its goals of optimizing store fleet, which resulted in significant store closures over the past eight years. The company takes these closures as an opportunity to improve store productivity by reducing store occupancy costs. Notably, the global store optimization is a key component of its efforts to deliver operating margin expansion and reach its goals for fiscal 2020.

As part of its continued focus on optimizing store fleet, Abercrombie announced plans to close three additional flagships. Apparently, it shut down Hollister SoHo in the reported quarter. The other two are Milan A&F that is expected to be closed by the end of fiscal 2019, and Fukuoka A&F in fiscal 2020.

Simultaneously, the company delivered 26 new store experiences in the reported quarter. It is currently on track to deliver about 85 new experiences in fiscal 2019.

Outlook

For fiscal 2019, Abercrombie now estimates sales to be flat to up 2% backed by comps growth and contributions from new stores. This will be somewhat offset by adverse impacts of currency to the tune of roughly $45 million, of which $26 million is reflected in the first-half results. Earlier, sales growth was projected in the band of 2-4%.

Further, comps are expected in the range of flat to positive 2% versus the earlier projection of growth in low-single-digits and 3% improvement in the year-ago period.

Operating expenses, excluding other operating income, are now expected to increase nearly 2-3% from adjusted operating expenses of $2.03 billion in fiscal 2018 compared with the prior view of 4-5% increase. The increase mainly reflects flagship store exit charges of about $45 million incurred in the reported quarter. Furthermore, it anticipates effective tax rate to be in mid-20s.

Additionally, Abercrombie continues to envision capital expenditure of roughly $200 million for fiscal 2019.

For the fiscal third quarter, the company anticipates sales to be up about 1% from the prior-year quarter. This includes an adverse impact of nearly $10 million from negative currency translations. Meanwhile, comps are anticipated to remain flat.

Operating expenses (excluding other operating income) are estimated to increase 1-2% from adjusted operating expenses of $493 million in third-quarter fiscal 2018. Excluding one-time charges in the prior-year quarter, adjusted operating expenses are likely to be flat to up 1%. Effective tax rate is anticipated in mid-to-upper 20s.

3 Key Picks in the Retail Space

Boot Barn Holdings, Inc. BOOT delivered average positive earnings surprise of 26.1% in the trailing four quarters. Currently, the stock sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Fossil Group, Inc. FOSL delivered positive earnings surprise of 79% in the last four quarters. The stock currently has a Zacks Rank #2 (Buy).

Shoe Carnival, Inc. SCVL has positive earnings surprise of 16.9% in the trailing four quarters and a Zacks Rank of 2.

Today's Best Stocks from Zacks

Would you like to see the updated picks from our best market-beating strategies? From 2017 through 2018, while the S&P 500 gained +15.8%, five of our screens returned +38.0%, +61.3%, +61.6%, +68.1%, and +98.3%.

This outperformance has not just been a recent phenomenon. From 2000 – 2018, while the S&P averaged +4.8% per year, our top strategies averaged up to +56.2% per year.

See their latest picks free >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fossil Group, Inc. (FOSL) : Free Stock Analysis Report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Shoe Carnival, Inc. (SCVL) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research