Yahoo Finance

Yahoo Finance These 4 Measures Indicate That Scotts Miracle-Gro (NYSE:SMG) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, The Scotts Miracle-Gro Company (NYSE:SMG) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Scotts Miracle-Gro

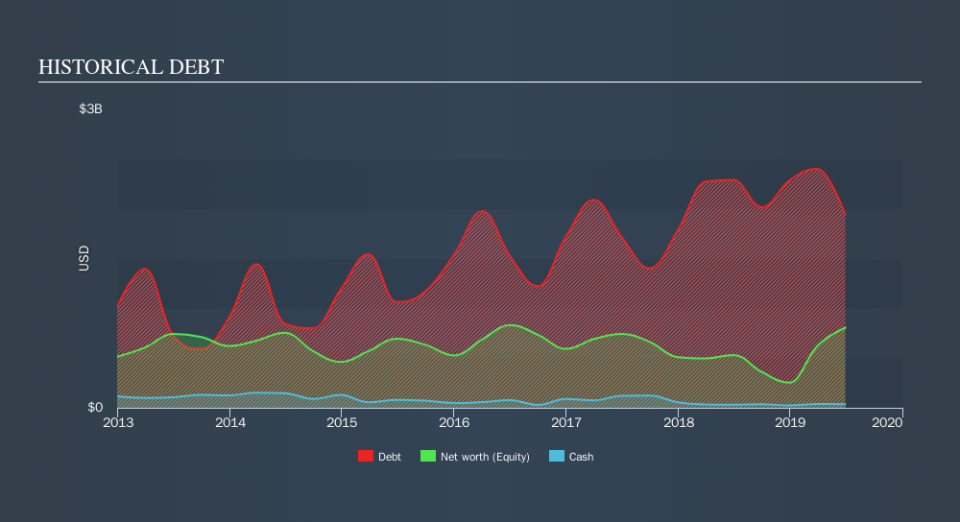

What Is Scotts Miracle-Gro's Net Debt?

The image below, which you can click on for greater detail, shows that Scotts Miracle-Gro had debt of US$1.94b at the end of June 2019, a reduction from US$2.29b over a year. And it doesn't have much cash, so its net debt is about the same.

How Healthy Is Scotts Miracle-Gro's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Scotts Miracle-Gro had liabilities of US$955.4m due within 12 months and liabilities of US$1.71b due beyond that. On the other hand, it had cash of US$36.4m and US$746.9m worth of receivables due within a year. So it has liabilities totalling US$1.88b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Scotts Miracle-Gro is worth US$5.65b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Scotts Miracle-Gro's debt is 3.6 times its EBITDA, and its EBIT cover its interest expense 4.7 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Also relevant is that Scotts Miracle-Gro has grown its EBIT by a very respectable 22% in the last year, thus enhancing its ability to pay down debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Scotts Miracle-Gro's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Scotts Miracle-Gro recorded free cash flow worth 59% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

When it comes to the balance sheet, the standout positive for Scotts Miracle-Gro was the fact that it seems able to grow its EBIT confidently. But the other factors we noted above weren't so encouraging. For example, its net debt to EBITDA makes us a little nervous about its debt. When we consider all the elements mentioned above, it seems to us that Scotts Miracle-Gro is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Scotts Miracle-Gro insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.