Yahoo Finance

Yahoo Finance 3 Top Renewable Energy Stocks to Watch

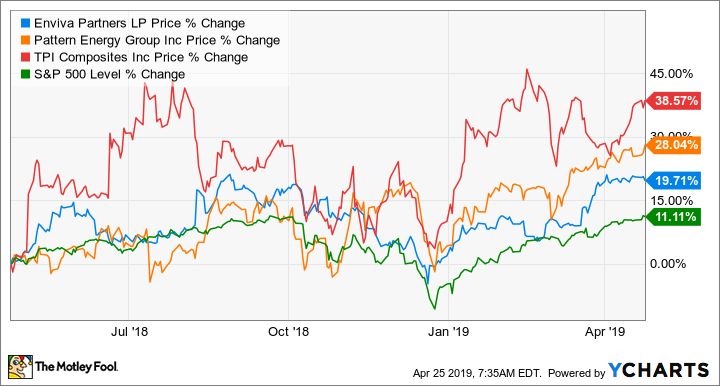

2019 has so far been a great year for renewable energy stocks. Rising energy demand coupled with lower interest rates has helped many stocks in this industry recover from less than stellar performances in 2018.

With the outlook for renewable energy looking great today, we asked three of our Fool contributors to each highlight a stock investors should have on their radar right now. Here's what they had to say about Enviva Partners (NYSE: EVA), Pattern Energy Group (NASDAQ: PEGI) and TPI Composites (NASDAQ: TPIC).

Image source: Getty Images.

Can this alternative-energy producer make good on its promises?

Tyler Crowe (Enviva Partners): Enviva Partners has been a fascinating company to follow in recent years. The manufacturer and exporter of pelletized wood chips has done a great job signing up customers to long-term takeaway agreements that ensures that almost all of the company's production capacity will have a buyer for close to a decade. It goes to show that wood pellets are an attractive alternative to coal as an energy source, where other renewable sources like wind and solar make less economic sense.

The company has faced a few hiccups over the past couple of years, though, between some operational issues at one of its processing facilities and hurricane damage to one of its ports. Those events resulted in a few quarters where the amount of cash it was paying investors was more than what the company could generate from operations. Fortunately, management was able to get back on track thanks to solid operations in the second half of 2018.

Recently, Enviva announced a major purchase of a new processing facility and port that will require it to issue new shares and issue debt. That's pretty normal for master limited partnerships, but management seems to think it can issue all these shares, grow its payout by double digits in 2019, and still generate enough cash to cover that payment by 1.15 to 1.2 times.

If it can pull that off all in 2019, then Enviva could look like an incredibly attractive renewable-energy option for investors.

When the wind blows

John Bromels (Pattern Energy): Pattern Energy isn't like most renewable-energy companies. It's a yieldco that develops and operates large-scale wind and solar farms -- mostly wind -- in the U.S., Canada, and Japan. As you'd expect from a yieldco, it also pays a monster dividend that's currently yielding about 7.4%.

The company has been trying to grow its dividend and its operations. But these goals came into conflict in 2018. Pattern upped its payouts to shareholders even as it was making acquisitions. When interest rates rose, the company experienced a bit of a cash crunch. It ended up paying out 99% of its 2018 cash flow as dividends. That doesn't leave much room for error, and it's well above Pattern's stated target of 80%.

Management believes it can right the ship without issuing new shares, while still growing its cash available for distribution by 10% annually for the next two years and making the acquisitions necessary to support this plan. In theory, the plan looks doable. In practice, it's not a slam dunk. For one thing, CEO Mike Garland admits that the bulk of the growth will come in 2020, as the company tries to move past some operational headwinds in 2019.

Given the uncertainty surrounding whether Pattern can pull off its grand plans, I'm not recommending buying the stock just yet, but it's definitely one to keep on your watchlist, especially if you like renewable energy and high yields.

Tilting at windmills

Rich Smith (TPI Composites): Tick-tock, tick-tock. April is winding down, and soon after the clock strikes "done" on this month, it will be time for wind-turbine blade maker TPI Composites to report its fiscal Q1 2019 earnings results. So far, March and April have already seen TPI shares make two attempts to climb out of their post-Q4 earnings funk. At nearly $31 a share this week, TPI stock has already hit its highest mark of the month.

But will the gains stick this time?

That may depend on how forgiving a mood investors are in on earnings day. Heading into Q1 2019 results, Wall Street is forecasting a nearly 80% decline in Q1 profits to just a nickel a share. On one hand, that sounds like TPI's report May 8 will be chock-full of bad news. On the other hand, it's an exceedingly low bar that the investment bankers have set for TPI -- especially given that they think TPI's sales are going to grow 16%. If sales grow as expected, I'd be surprised to see earnings as weak as Wall Street is projecting.

As a shareholder, of course, what I'd really like to see is a return to positive free cash flow at this windmill blade-maker, 2018's $56 million in cash-burn having been a disappointing way to end the year. For me, that will be the real "buy signal," -- and it's the reason I'll be waiting until May to decide whether to buy more shares.

More adventurous investors, however, might want to roll the dice, buy TPI in April -- and hope for a pleasant surprise come May.

More From The Motley Fool

John Bromels has no position in any of the stocks mentioned. Rich Smith owns shares of TPI Composites. Tyler Crowe has no position in any of the stocks mentioned. The Motley Fool recommends TPI Composites. The Motley Fool has a disclosure policy.