Yahoo Finance

Yahoo Finance 3 Things Baytex Energy Corp. Has to Prove in 2017

Baytex Energy Corp. (TSX:BTE)(NYSE:BTE) entered 2017 with more optimism than it has had in quite some time. That?s evident by the company?s growth-focused capex budget, which will see the company reverse a steady string of spending cuts. However, despite the more bullish tone to start the year, the company has plenty to prove before investors will have the confidence that this company is back on the path towards sustainable growth.

No. 1: Demonstrate the sustainability of its cost reductions

One of the reasons Baytex Energy could boost spending this year is due to a significant improvement in its cost structure. For example, operating expenses are down 30% per barrel of oil equivalent (BOE), while transportation costs have fallen 33% per BOE. Those reductions will help the company generate more cash flow per barrel at current prices than it would have otherwise.

At the same time, drilling costs in the Eagle Ford are down 40%, enabling the company to drill more wells with the same amount of money. Because of these cost savings, the company can drill enough wells to maintain its current output level at $55 oil, which is a dramatic improvement in its breakeven point.

That said, many of these cost reductions have come at the expense of oilfield-service companies, which have cut their prices. For example, drilling contractor Precision Drilling Corp. (TSX:PD)(NYSE:PDS) only collected $654 in revenue per operating hour last year, which is down 17.3% year over year. Driving the decline was the fact that fewer rigs were drilling last year due to lower prices.

However, as more oil companies start adding rigs, it will likely drive service prices higher as producers compete against each other for the best rigs. Given this backdrop, Baytex Energy needs to prove that most of its costs reductions will stick even as service prices begin rising.

No. 2: Show that it can continue to improve its balance sheet

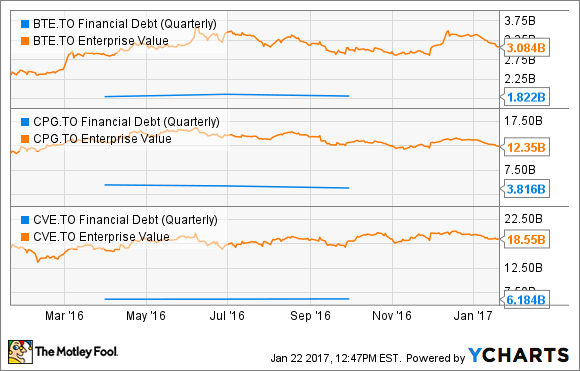

Another of Baytex Energy?s aims during the downturn was to maintain a healthy balance sheet. The company did this by generating excess cash flow and selling non-core assets, using the money to pay down debt. Thanks to these efforts, net debt declined 11% last year to $1.8 billion.

While that?s an improvement, Baytex Energy still has too much debt for a company of its size. That?s evident by the fact that debt makes up nearly 60% of the company?s enterprise value. Contrast this with larger rivals Crescent Point Energy Corp. (TSX:CPG)(NYSE:CPG) and Cenovus Energy Inc. (TSX:CVE)(NYSE:CVE), which have debt levels between 30% and 33% of their enterprise value:

Given its larger debt load, Baytex Energy needs to continue to improve its financial situation. Among its options are selling additional non-core assets or issuing equity, which are the paths taken by Cenovus and Crescent Point to strengthen their balance sheets during the downturn.

No. 3: Deliver on its growth promise

Baytex Energy plans to spend between $300 million and $350 million this year, which is enough capital to boost its production 3-4% by year-end. That guidance is a significant improvement over last year when the company was only able to spend $225 million, which wasn?t nearly enough capital to maintain its 2015 production level. In fact, through the third quarter, production was down more than 17% year over year.

For Baytex Energy?s 2017 plan to be a success and reverse that production slide, two things must happen. First, oil needs to stay above $55 per barrel, which is the price point that would enable it to generate enough cash flow to finance its capex budget internally. Second, the company needs to keep a lid on costs, so they do not re-inflate. Otherwise, the company runs the risk of failing to deliver on promised growth, which could weigh on the stock.

Investor takeaway

Baytex Energy believes it is back on firm footing and can run sustainably at lower oil prices. That said, the company still needs to prove that this is the case. To do so, it must demonstrate that its cost reductions will stick in the recovery, while it also delivers further balance sheet improvements and makes good on its promise to grow production. The company?s ability to achieve all three aims should prove to investors that it really is back on solid ground.

You've probably never even heard of this up-and-coming e-commerce powerhouse headquartered in Eastern Ontario...

But, despite coming public just last year, it's already helping the likes of Budweiser... Tesla... Subway... and Red Bull move $9.9 BILLION (and counting) worth of goods online each year.

And now it's caught the eye of the legendary investor who got behind Amazon.com in 1997 -- just before it shot up over 23,000% and made investors like you and me rich beyond their wildest dreams.

Click here to discover why this investor says it's time to buy.

More reading

Fool contributor Matt DiLallo has no position in any stocks mentioned.

You've probably never even heard of this up-and-coming e-commerce powerhouse headquartered in Eastern Ontario...

But, despite coming public just last year, it's already helping the likes of Budweiser... Tesla... Subway... and Red Bull move $9.9 BILLION (and counting) worth of goods online each year.

And now it's caught the eye of the legendary investor who got behind Amazon.com in 1997 -- just before it shot up over 23,000% and made investors like you and me rich beyond their wildest dreams.

Click here to discover why this investor says it's time to buy.

Fool contributor Matt DiLallo has no position in any stocks mentioned.