Yahoo Finance

Yahoo Finance Here are the big stories that will drive the stock market in 2020

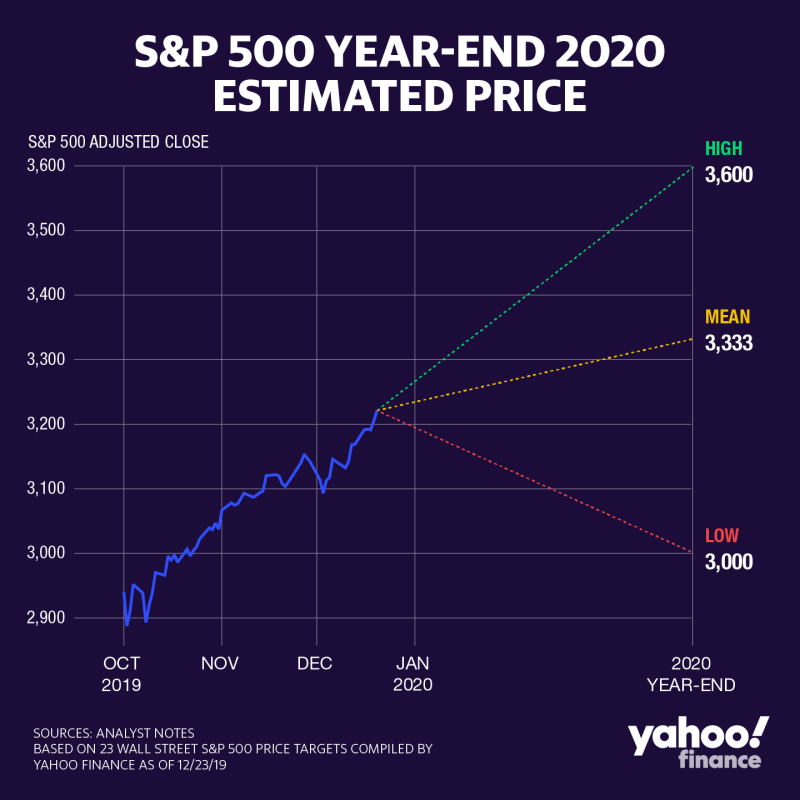

As trading kicks off in 2020, most major Wall Street firms have delivered their early expectations for where equities are headed in the new year.

So far, most have been optimistic. Twenty of 23 financial institutions’ predictions reviewed by Yahoo Finance suggested the S&P 500 would end at least marginally higher in 2020, after closing out 2019 nearly 29% higher on the year at 3,230.78.

Here’s a look at some of the major themes underpinning Wall Street’s expectations for equity trading this year.

Trade war, Brexit risks shrink

Two events in December nearly simultaneously lowered the fear gauge on some of the biggest overhangs for stocks last year.

First, the Trump administration and China each said they had reached and would sign a phase one trade agreement, with is now on track to be signed later this month. And second, U.K. Prime Minister Boris Johnson’s landslide election win provided some much-needed clarity on a path forward for Brexit.

While both events still carry a risk of taking a turn for the worse, strategists have by and large factored in more positive sentiment surrounding these headline-dominating factors in making their 2020 predictions.

“Global business sentiment should start to heal and help normalize investment activity including inventory restocking as fears related to US/China trade, Brexit, and other one-off shocks to large economies fade (e.g. Italy, India, etc.),” JPMorgan strategist Dubravko Lakos-Bujas wrote in a Dec. 9 note. “All of the above leads us to believe that the business cycle should begin to gain stronger traction by early 2020.”

And as risks surrounding both Brexit and the U.S.-China trade war abate, investors will be free to focus on “the traditional drivers of markets” and especially earnings growth, Jefferies strategist Sean Darby said in an early December note. S&P 500 earnings per share (EPS), in turn, has the back of a strengthening economic backdrop, with late-2019 data pointing to a resilient labor market, thumping consumer spending and firming housing market.

“Looking toward 2020, the outlook for growth and risk assets has improved. Global economic growth, though still stuck in low gear, has started to improve. Earnings growth is set to reaccelerate,” said Dennis DeBusschere, Evercore chief investment strategist.

2020 elections

But as 2019’s risks diminish, new concerns will take their place – and many strategists count the 2020 U.S. elections as one such area to watch.

An outcome that sees a Democratic candidate take the White House could pose a risk to some sectors in the event that new sweeping policies replace those of the current administration, some analysts said.

Namely, companies within the health-care, financial and energy sectors are most at risk as an election outcome holds in abeyance, said Ned Davis strategist Pat Tschosik.

Highlighting just one candidate’s policy goals as an example, Tschosik said these sectors could “stand to decline if Elizabeth Warren’s stated policies were implemented, including: her desire to end offshore drilling and drilling on federal land, reduce greenhouse gases, increase regulation on big banks, impose regulation on private equity, control drug prices, make the U.S. government the sole health-care insurance payer, break up big tech companies, increase gun control and reallocate/reduce defense spending.”

However, “as election winners become clear, we expect some sectors to mean revert to their normal valuation as political risk is priced out,” he added. “Again, we suspect health care, financials and energy are likely to have the most political risk priced in, creating a buying opportunity.”

That said, Tschosik’s base case outlook — as well as that of a number of other Wall Street strategists — assumes Republicans will control of at least one of the Senate or White House post-election, which could make implementation of new policies more difficult.

Others assigned a low weight on the impact of the elections for U.S. equity returns, with JPMorgan’s Lakos-Bujas saying he did “not think that U.S. elections are a key risk that should keep investors out of risk markets.

“In terms of US Presidential Elections, we think that the two most likely outcomes are Trump’s re-election or an experienced centrist Democrat, which would be neutral or positive for markets (at least initially),” he said. “A progressive left Democratic candidate could be a significant downside risk for the market; however, we assign a low probability to this outcome.”

Fed pause

The Federal Reserve’s dovish pivot was a major driver of stock market gains in 2019, with falling interest rates sending investors scuttling for yields and into equities. And as an added bonus, the Fed re-started its balance sheet expansion, making large-scale asset purchases and pumping liquidity into financial markets.

With Fed officials having telegraphed rates would likely remain in place through 2020 at a relatively low target range of between 1.50% to 1.75%, domestic monetary policy is poised to continue being a tailwind for stocks this year.

“The generational change in how the Fed views inflation has been made clear by Fed Chair Powell who literally told us the Fed is going to remain on the sidelines for the foreseeable future, which gives us an offensive playbook,” Canaccord Genuity analyst Tom Dwyer said in a note Dec. 9. “They have clearly stated they are keeping rates low until there is a meaningful ramp in inflation vs. a fear of one. As a result, we believe any market weakness should prove limited and temporary.”

Such an accommodative stance has also been reflected in moves by other central banks around the world during 2019, including the European Central Bank and Bank of Japan. The result has been a globally coordinated low-rate environment and resounding message that central bankers have an eye on keeping stimulus in place as needed amid low inflationary signals.

“Led by the Fed reversing course this year, we have argued that the change in trajectory of global monetary policy will be a powerful driver of a new intracycle recovery, a third reset for an expansion already the longest since 1860,” JPMorgan’s Lakos-Bujas said. “The proportion of global central banks in easing mode has doubled to ~80% from ~40% in April. Historically, this leads an upturn in global manufacturing by 6 to 9 months.”

Late-2019 style and sector rotation

Starting in late August and continuing through the fourth quarter of 2019, investors began piling into value stocks, or those considered “cheap” relative to fast-appreciating momentum stocks. The rotation also spilled over to cyclical stocks, or those that tend to follow an upward trend in tandem with an improving economy, amid a bottoming in bond yields in August and positive turn in U.S.-China trade talks and improvement in economic data.

Many strategists believe this style and sector rotation will continue at least through the start of 2020.

“Our 2020 game plan is to continue the transition toward cyclical-value equities/sectors,” Scotiabank strategist Hugo Ste-Marie said in a note Dec. 3. “The outsized value reversal seen last September was relatively rare and these tend to be followed by value outperformance over the next 12 to 18 months.”

JPMorgan’s Lakos-Bujas was even more specific, and said last month he expected the rotation out of momentum and into value stocks had only “partially corrected the extreme dislocation among styles.”

“History implies that the current Momentum/Value rotation is ~40% complete,” he said. “We prefer relative Value plays within Cyclicals, Growth and Defensives, which should benefit from global synchronized recovery and diminishing trade headwinds.”

—

Emily McCormick is a reporter for Yahoo Finance. Follow her on Twitter: @emily_mcck

Read more from Emily:

Stock Market 2020: BMO’s bull is reminded of Notorious B.I.G., Tupac and Snoop

How this CBD company created a buzz by ‘kind of making fun of millennial culture’

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and reddit.

Find live stock market quotes and the latest business and finance news