Yahoo Finance

Yahoo Finance Can Aaron's (AAN) Plans Counter the Sluggish Demand Trends?

The Aaron’s Company, Inc. AAN has been on track to expand its e-commerce business, driven by its omni-channel lease decisioning and customer acquisition program. This program has been resulting in improved lease portfolio size, which was evident in the first quarter of 2024. Despite a year-over-year decline, the company’s lease portfolio size marked a sequential improvement of 220 bps in the first quarter.

Additionally, AAN is focused on the implementation of its GenNext strategy and its cost-reduction measures aimed at improving efficiency and strategic procurement. At BrandsMart, the company plans to enhance its capabilities in merchandising, marketing and technology to better position the business for long-term growth.

However, Aaron’s faces several challenges. The company has been impacted by changing market dynamics, which are expected to continue in the near term. It deals with soft retail sales and stiff competition. AAN has been, particularly, witnessing sluggish demand for discretionary products that led to a soft top-line performance in first-quarter 2024.

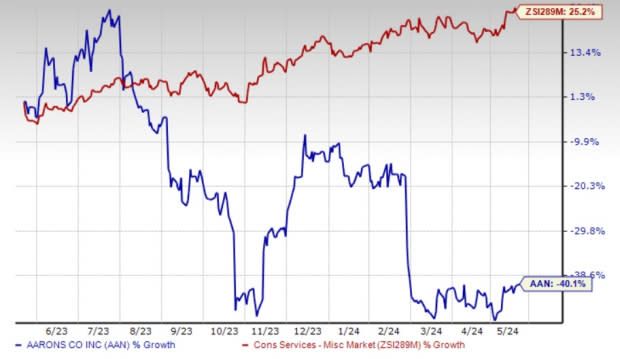

Driven by the soft performance, shares of this Zacks Rank #3 (Hold) company have lost 40.1% in the past year against the industry’s growth of 25.2%. The Zacks Consensus Estimate for current fiscal-year sales and earnings indicates declines of 1.7% and 84%, respectively, from the year-ago reported levels.

Image Source: Zacks Investment Research

Initiatives to Watch

Aaron’s has been displaying strength in its e-commerce business, driven by flexible payment options, low prices and a wider variety of products. Some other notable efforts include increased investments in digital marketing, improved shopping experience, same-day and next-day delivery facilities, the personalization of products, and a broader assortment, including the latest product categories. Its express delivery program also bodes well.

Driven by these, revenues generated from leases initiated on Aarons.com improved 20.8% year over year in first-quarter 2024 and represented 24% of lease revenues for the Aaron’s business. Recurring revenues written into the portfolio from e-commerce improved 94.1% year over year, gaining from new omni-channel lease decisioning and the customer acquisition program. This represented 34% of the total recurring revenue written in the quarter.

Aaron’s latest acquisition of appliance and electronics retailer BrandsMart has been gaining from better cost controls, strategic procurement and pricing actions. At BrandsMart, the company remains focused on improving the shopping experience by rationalizing its product assortments, expanding its furniture product mix and investing in digital marketing strategies to attract customers. The company is also on track to enhance its capabilities in merchandising, marketing and technology to better position the business for long-term growth. Also, cost-optimization initiatives at BrandsMart bode well.

Although the broader demand environment is still challenging, management remains confident in BrandsMart's compelling value proposition and potential to expand to new markets. Management expects improved demands at BrandsMart in the second half of the year mainly due to the anticipated rebound in the product categories. For 2024, BrandsMart revenues are anticipated to be $610-$650 million, whereas the adjusted EBITDA is forecast at $7-$12 million.

Sluggish Financial Performance

In the first quarter of 2024, Aaron's faced a notable downturn in its financial performance. Consolidated revenues declined 7.7% year over year in the first quarter, driven by soft lease revenues and fees at the Aaron's business, and a dip in retail sales at the BrandsMart business.

Aaron’s has been witnessing elevated operating costs mainly related to increased investments in advertising and higher provision for lease merchandise write-offs. This has been mainly hurting the bottom line and adjusted EBITDA. In the first quarter of 2024, the company’s total operating expenses rose 1.2% year over year, mainly on a 6.3% rise in other operating expenses (including advertising costs) and a 1.7% increase in provision for lease merchandise write-offs.

Additionally, the provision for lease merchandise write-offs, as a percentage of revenues, increased 50 bps due to the increasing mix of e-commerce agreements written into the portfolio. For 2024, the company expects the provision for lease merchandise write-offs between 6% and 7% of lease revenues and fees.

Given the ongoing soft demand environment and uncertainty, the company reaffirmed its 2024 outlook for revenues and adjusted EBITDA. For 2024, AAN anticipates revenues of $2.055-$2.155 billion, whereas the adjusted EBITDA is projected to be $105-$125 million.

Stocks to Consider

Some better-ranked companies in the Consumer Discretionary sector are Hanesbrands HBI, Crocs CROX and H&R Block HRB.

Hanesbrands engages in the design, manufacture, sourcing and sale of apparel essentials for men, women and children in the United States and internationally. The company currently sports a Zacks Rank #1 (Strong Buy). It has a trailing four-quarter earnings surprise of 10.2%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Hanesbrands’ current financial-year earnings suggests significant growth of 650% from the 6 cents reported in the prior year. The consensus mark for HBI’s earnings per share has moved up by a penny in the past 30 days.

Crocs, one of the leading footwear brands with its focus on comfort and style, currently carries a Zacks Rank #2 (Buy). CROX has a trailing four-quarter earnings surprise of 17.1%, on average.

The Zacks Consensus Estimate for Crocs’ current financial-year sales and earnings suggests growth of 4.4% and 5.2%, respectively, from the year-ago reported numbers. The consensus mark for CROX’s earnings per share has moved up 1.6% in the past 30 days.

H&R Block, a leading provider of tax preparation services, currently carries a Zacks Rank #2. HRB has a trailing four-quarter earnings surprise of 10.3%, on average.

The Zacks Consensus Estimate for HRB’s current financial-year sales and earnings suggests growth of 3% and 12.3%, respectively, from the year-ago period’s actuals. The consensus mark for HRB’s earnings per share has moved up 0.9% in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Aaron's Company, Inc. (AAN) : Free Stock Analysis Report

Hanesbrands Inc. (HBI) : Free Stock Analysis Report

H&R Block, Inc. (HRB) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report